Credit Agricole investment bank’s analysts presenting their views and forecasts for the year ahead in the 2020 FX Outlook.

Key FX Views & Forecasts Update

- We expect many of the risks that plagued the global economy in 2019 to intensify in 2020. We expect global growth to be weaker, dragged down by lingering protectionist threats and, in the case of the US, political risk ahead of the 2020 presidential elections. The risk of a global recession could increase. In comparison to 2019, we expect the US to be the main contributor to the slowdown, whereas the likes of the Eurozone and China could see some consolidation.

- The resulting convergence between the cyclical outlooks for the US and the rest of the world could accelerate the policy convergence between the Fed, which is expected to cut rates again in 2020, and the ECB and the BoJ, which we believe are close to the bottom of their easing cycle.

- The USD is still the undisputed King of FX. This should remain the case as long as it commands a significant rate advantage over its peers and offers superior liquidity during bouts of risk-off. That said, in our view, the erosion of the USD’s rate advantage and growing US political risks could weigh on the currency vs the EUR and JPY as well as the GBP in 2020. The weakness could be temporary, however, and we see the USD regaining ground in 2021, assuming that the status quo is preserved after the presidential election and the US economy regains its footing.

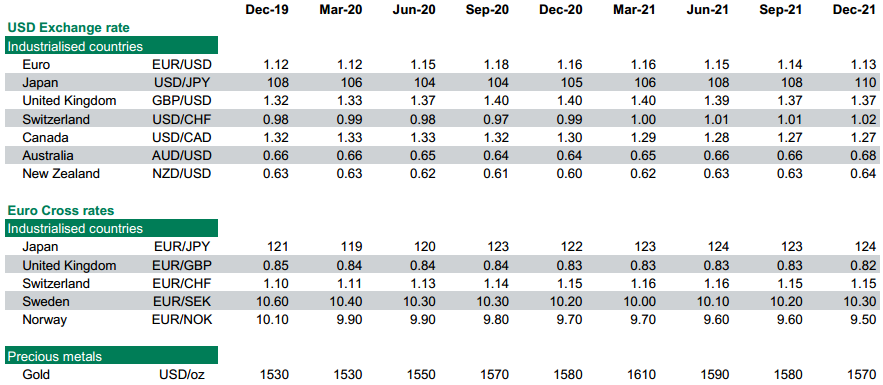

- The EUR should remain an attractive funding currency because of the ultra-low yields in the Eurozone. We expect the undervalued and oversold EUR/USD to strengthen somewhat in 2020, however, as the Eurozone economy consolidates and the downside risks to the US outlook intensify. We see EUR/USD at 1.16 in Q420 and at 1.13 in Q421.

- The JPY remains oversold and undervalued and could regain some ground vs the USD as investors unwind carry trades in the next six to nine months. We see USD/JPY at 105 in Q420 and 110 in Q421. The GBP should be the best-performing G10 currency in 2020 in our view, on the back of abating Brexit risk. We see GBP/USD and EUR/GBP at 1.40 and 0.83 in Q420 and 1.37 and 0.82 in Q421 respectively.

- We see AUD/USD, NZD/USD heading lower in H120 (AUD/USD to 0.64 and NZD/USD to 0.60) as their central banks loosen monetary policy by cutting rates and potentially implement unconventional monetary policies in H220. The CAD should recover in earnest only in H220, and we see USD/CAD at 1.30 in Q420 and 1.27 in Q421.

- We see EUR/CHF at 1.15 in Q420 and Q421. We see EUR/SEK and EUR/NOK at 10.20 and 9.70 in Q420 and at 10.30 and 9.50 in Q421 respectively. We are bullish gold and expect it to reach 1580 in Q420 and 1570 in Q421.

2020 FX Outlook – key trade views:

- Unwinding of USD carry trades: long EUR/USD via 6M-9M options, target 1.16; short USD/JPY, target 105

- The end of Brexit: long GBP/USD, target 1.36 and GBP/CHF, target 1.35

- Commodity carry trade: long CAD/CHF, target 0.80

- Trade war hedges: Long XAU/USD, target 1600 and long USD/SEK, target 11, Sell AUD/JPY 6M risk reversal

Latest forex analysis and forecast updates from major banks are available to our regular subscribers. Subscribe now or get a free 5-day trial.

2020: the year of living dangerously

We expect the global economy to continue to slow down in H120 before consolidating later on and into 2021. This partly reflects the view that US-China trade tensions could resurface, following a successful completion of the phase-one deal in the coming months. Credit Agricole CIB’s economists further think that, compared with 2019, the main contributor to the global economic slowdown will be the US. Indeed, they expect the economy to decelerate sharply in H120 due to abating positive impact from past fiscal stimulus, softer business sentiment and consumer confidence and growing political uncertainty ahead of the US presidential election.

Elsewhere, our economists expect the European growth outlook to stabilise in 2020, thanks to the monetary and fiscal stimulus as well as abating political risks (eg, Brexit). The European growth rates should remain rather subdued, however. Furthermore, monetary and fiscal stimulus should help stabilise Chinese economic growth at a historically low level as well . While Japan, Australia and New Zealand could benefit from easier domestic financial conditions, the risk of further RBA and RBNZ easing should remain material in our view.

A cyclical convergence between the US and other major economies in 2020 should spur up a monetary policy convergence according to Credit Agricole CIB’s economists. We expect the Fed to cut rates again in Q220. At the same time, the ECB and the BoJ may not be that far off from the bottom of their respective easing cycles. We further believe that unstable global risk sentiment next year, against the backdrop of weak global growth outlook and persistent geopolitical risks, could add to the pressure on the Fed to ease further as well.

2020 FX outlook – G10

The USD remains the currency with the greatest rate and yield advantage in G10, and this makes us constructive in the near-term especially if more progress towards a US-China trade deal boosts demand for USD carry trades. That said, the cyclical and policy convergence between the US and the rest of the G10 could intensify, as the US economy slows down further in H120 and political risks intensify ahead of the US presidential election. Another Fed rate cut and a balance sheet extension could add to the downside risks for the overvalued and overbought USD in the next six to nine months as investors unwind USD carry trades. Our expectation of lacklustre USD performance is further consistent with the FX price action in the wake of the previous “mid-cycle rate adjustment” that the Fed delivered in Q498 and that was followed by an extended pause in rates for most of 1999.

We forecast a modest EUR recovery in the next six to nine months. The view reflects the fact that the currency remains very oversold and undervalued – all factors that could help it recover as EUR-funded carry trades are unwound in the face of stabilising Eurozone and deteriorating US outlook. The risk of “Japanification” of the Eurozone should contain any EUR gains over the long-term, however, by keeping the domestic investors invested abroad for longer.

The JPY has relinquished some of its recent gains as 2019 draws to a close, as risk sentiment improved on the back of hopes that the US and China are moving close to a trade deal. This has little impact on our constructive longer-term outlook for the currency, however. Indeed, market concerns that the Bank of Japan is at the rock bottom of its easing cycle as well as significant JPY undervaluation and market shorts (JPY-funded carry trades) seem to all point to renewed JPY gains in the next six to nine months.

Our economists expect no-deal Brexit risks to abate after the 12 December general election. This should help support the GBP and make it the best-performing G10 currency in 2020. The CHF remains very overvalued while the Swiss National Bank’s dovish stance looks to be here to stay, painting a bearish picture for the CHF in 2020. The SEK and NOK should recover gradually in 2020, as the Riksbank normalises rates and the Norges Bank remains among the few G10 central banks with a neutral policy stance.

We expect the AUD and NZD to remain vulnerable in 2020 as a dovish RBA and RBNZ add to global headwinds. We expect trade war concerns to resurface in the coming quarters and add to the headwinds for the two currencies. Compared to the other G10 commodity currencies, the CAD should remain relatively more resilient in 2020, supported by BoC policy outlook, oil prices and the ratification of USMCA. We remain bullish gold looking going into 2020 and beyond.

2020 G10 FX and gold forecasts

Latest forex analysis and forecast updates from major banks are available to our regular subscribers. Subscribe now or get a free 5-day trial.