J.P.Morgan Key Currency Views – USD more than just a one quarter wonder

- G10 FX continues to be driven by USD-supportive interest rate divergence, while EM has enjoyed stable US real yields and stronger global growth over the past month, punctuated with a series of idiosyncratic events.

- Biden’s fiscal plans and focus on Treasury supply are expected to keep higher US yields a recurring source of support for the dollar.

- Our view is unchanged. USD strength is best positioned versus currencies where the central bank is likely to remain dovish…

- …while high beta longs should be selective and funded via EUR, JPY, CHF.

- Global FX carry baskets have delivered positive returns and commodity FX have been resilient amid higher US yields and benign global growth.

- Stay long USD in G10 vs. vulnerable low yielders (EUR, CHF, JPY, Antipodeans). G10 high beta longs remain limited to NOK and CAD.

- In EM, our strategists have been cutting exposure and are neutral overall with a preference for Latam (via COP, MXN). We are now underweight Asia and EMEA, having closed overweights in CNY and RUB this week.

- G10 FX projections unchanged except USD/JPY (1y 106 from 104 on higher US yields). Key 1Q’22 targets: EUR/USD 1.16, USD/CAD 1.22, GBP/USD 1.36, AUD/USD 0.71, EUR/NOK 9.80.

- EM: CNY downgraded on US exceptionalism. 2Q USD/CNY at 6.65 (from 6.35), 6.50 by year-end (from 6.35). USD/RUB revised higher on geopolitical tensions (1y 74 from 70). USD/MXN (year-end 21.50), USD/BRL (5.45) and USD/ZAR (16.0) unchanged.

Global FX carry baskets have delivered positive returns amid higher US yields and benign global growth

J.P.Morgan Forex Forecast 2021

for Major Currencies

EUR Forecast 2021

Gaps in growth and yield should depress EUR/USD for longer than just one quarter

The euro is enjoying a better start to 2Q having struggled with a resurgent USD through 1Q. Indeed, the two cents bounce so far in April has already erased a third of the prior 5% drop. The speed of EUR’s retracement may be impressive but in our opinion it lacks a convincing fundamental basis and so should be regarded as a technical retracement rather than the beginning of a durable trend reversal. We are making no changes at this juncture to either our moderately negative EUR/USD forecast – the 1Y remains at 1.16 – or our short EUR trade recommendations.

April has delivered some nasty price action in certain currencies, most notably the sharp declines in RUB, INR and also GBP. And to the extent that clients may have adopted similar strategies to ourselves, namely the use of the euro as the funding currency for selective high-beta longs, this unwind of populated positioning may in part explain the bounce in the single currency. But EUR-funding is by no means deeply engrained – indeed the IMM data continues to show there is still a net speculative long in EUR, albeit one that is two-thirds down from the peak last summer – and as such we very much doubt whether short covering alone can drive material gains in EUR/USD over and beyond 1.20.

Whether EUR/USD is close to bottoming-out in a more durable sense hinges instead on whether those fundamentals that have pulled the euro back to earth over the past few months – the gap in growth expectations and yields that has opened up between the US and the Euro area – are themselves close to reversing; in short whether we are at, or close to, the point of peak US-exceptionalism. Certainly much, if not most, of the good news about US fiscal policy should by now be embedded in economic excitations. But that doesn’t mean to say that growth expectations are bound to reverse in EUR’s favour now. Similarly, while Europe is finally managing to increase the pace of vaccinations, this alone will not suffice to lift economic expectations since surely nobody doubted that Europe will eventually get to re-open its economy, just that this would be delayed by a month or two (for instance our economists downgraded 2Q in response to the extensions of lockdowns but put back most of that lost growth into 3Q). A material recovery in EUR/USD is hence likely to require not merely that Europe re-opens more fully by May/June, albeit this could provide temporary support, but that growth bounces more vigorously-than-expected when it does so. It is also likely to require that the US economy disappoints in outright terms and fails to reach the heady heights of 10%+ growth that our economist believe is feasible in both 2Q and 3Q.

J.P.Morgan forex forecast updates as well as major investment banks’ forecasts are available to our regular subscribers. Subscribe now or get a free 5-day trial.

JPY Forecast 2021

Marking up the USD/JPY outlook across the forecast horizon

USD/JPY’s repricing alongside US rates necessitates a shift higher in the profile: we are marking up the USD/JPY forecast by 1-2 yen (2Q21: 108; 1Q22: 106). JPY is almost flat versus the USD since the last publication of KCV, in line with what has essentially been a round-trip in US10Y yields through the past several weeks, and leaving it second to CHF in terms of G10 performance versus USD. Indeed, USD/JPY’s relationship with nominal yield spreads has remained extremely tight, something that does not typically persist over the course of several months. Spot at these levels looks fair relative to the year-to-date relationship with the UST-JGB 10Y yield differential; indeed its short-term rolling correlation with rates spreads has risen to extreme highs, in part reflecting spec JPY positioning (at least as proxied by IMM data) that has for the most part caught up with the direction and speed of US yield moves.

But correlations between the UST-JGB yield spread and USD/JPY are unlikely to remain as high into 2Q. We think the potential for a cooling in spec positioning in line with a potentially more orderly pace of US yield rises, re-emergence of two-sided Japanese direct investment flows (discussed below), and lack of fresh unhedged portfolio investment outflows should combine to give the yen some support versus the USD, though another sharp repricing higher in US rates similar to the 1Q experience would challenge this view. From a medium-term vantage point, valuations continue to look attractive for JPY: even with the backup in US rates so far this year, the yen still looks around 10% cheap to a medium-term metric of fair value versus the USD, with fair value currently sitting around the low-90 handle based on the long-term relationship to 10Y US-Japan real yield spreads.

Direct investment flows look set to become a more important variable for the yen given several large M&A deals in the pipeline, both into and out of Japan. The implication here is that USD/JPY’s near perfect year-to-date correlation with nominal yield spreads is unlikely to sustain if direct investment flows continue to pick up. Japan’s direct investment collapsed through 2020, but has gradually recovered through early 2021: net direct investment outflows remain relatively small, but net outflows in the three months through February more than doubled their pace over the prior three months. On the flip side, scope for large direct investment inflows also suggests that, if accompanied by yen demand, these flows could contribute to a loosening in USD/JPY’s relationship with rates differentials this quarter, giving JPY a tailwind even in the face of US yield rises.

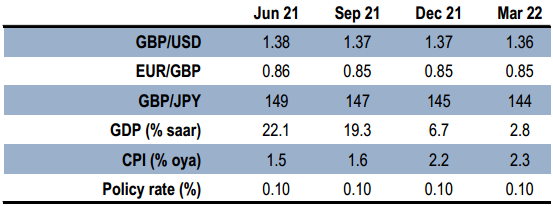

GBP Forecast 2021

Winning the vaccination race was only ever going to be a short-term GBP boost

Even though we upgraded our GBP forecasts last month to reflect the head-start that the UK’s vaccination programme will give the economy in opening-up, we cautioned that this was only ever likely to provide a transitory lift for GBP. And indeed, with the US starting to catch-up with the UK, and even the EU starting to make inroads into its vaccination programme (the UK has vaccinated 55% of its population, the US 51% and the 14 EU 19%), chances were that the vaccination premium in GBP would start to fade, especially considering that the speculative market had uniquely held onto long GBP positions even as USD shorts were aggressively cut versus other currencies. We consequently kept a modest negative profile for the cable forecasts and accompanied this with an outright short trade recommendation in the pound. There are no additional changes to the GBP forecasts this month – 1Y cable is set at 1.36 – and we continue to hold a short position in cable, which is now modestly in the money following evidence this week that investors are finally starting to rotate out of vaccine leaders such as GBP.

With vaccinations now fading as a driver of GBP, investor attention should turn to the sustainability of economic growth following the boom that will inevitably accompany the economic re-opening. And on this f ront we remain a skeptical about whether the UK is capable of sustaining any real degree of outperformance given the fiscal drag in the UK (1.8-ppt according to the IMF) as well as the still uncertain damage from what in theory was a relatively hard Brexit, especially for UK service-sector exporters (all countries have Covid to contend with, only the UK has Brexit). And with the Scottish parliamentary elections now just a month away, there is a secondary negative for GBP to consider, namely the political pressure for a second referendum on Scottish independence against a backdrop in which opinion polls show roughly 50% support for independence (the 2014 referendum rejected independence by a margin of 55-45%).

The GBP rate market concurs with our analogy of the UK economy as a sprinter, one that will be fast out of the blocks but which has questionable stamina. The result – BoE tightening is priced close to the Fed for the first couple of years (the first 25bp hike is priced in two years for both the BoE and Fed versus four years for the ECB) but closer to the ECB thereafter (cumulative tightening through the cycle is priced at 120bp for the BoE, 110bp for the ECB, and 230bp for the Fed). So while the UK’s vaccination strategy has improved the prospects for rate lift-off, the structural drag from Brexit continues to depress perceptions of the terminal rate in the UK, and it is the latter which should ultimately serve to restrain GBP over a multi-quarter horizon.

CHF Forecast 2021

Growth and rate diffs remain bullish for USD/CHF; EUR/CHF is more neutral

The franc has recovered slightly over the past month following what was a pretty intense phase of depreciation in February. Our forecasts continue to expect modest additional depreciation in the franc over the coming year, but we emphasise that this should be confined to the most part against the USD, where there is a genuine growth and interest rate justification. EUR/CHF, by contrast, lacks any realistic prospect of a reversal of the incessant compression, indeed elimination, of rate differentials that has been underway since the GFC and which has eliminated any incentive for unhedged capital flows from CHF to EUR. The 1Y forecast for USD/CHF is unchanged from last month at 0.97; EUR/CHF is kept at1.12. The one slight change to the forecast is that the peak in EUR/CHF is trimmed from 1.13 to 1.12 – last month we were unsure how far the momentum in EUR/CHF would extend and hence allowed for a certain degree of overshoot. As it turned out, momentum has stalled as quickly as it emerged, confirming that the policy environment is not what it was in 2017, when there was a genuine prospect of the ECB hiking rates which lifted EUR/CHF 12% to 1.20.

Our basic framework for thinking about CHF continues to emphasise the essential anti-cyclicality in the currency. Contrary to conventional wisdom this is not defined by the franc’s sensitivity to risk markets – CHF has appreciated hand-in-hand with the record bull market in equities for over a decade now. Rather, the trend appreciation in the currency can be linked to the persistent shortfall in global growth since the GFC. Indeed, the cumulative downgrade in global growth expectations explains a full 90% of the performance of the franc over the past 15 years. As such, it is not unreasonable to suppose that there is scope for CHF to give back some of that trend appreciation as the global economy stands on the cusp of the strongest growth in at least the last 50 years bankrolled in part by the biggest US fisca experiment in peace-time. One can question the sustainability of this growth, for sure, and hence it is premature to think about a full structural reversal in the CHF TWI. But over the 1Y horizon of our forecasts, growth should be robust and sustained enough (assuming no unmanageable mutation in the virus, of course) to bear down somewhat on the franc’s elevated valuation levels (the CHF REER is 3% above its 20Y average, the highest level amongst the G10 currencies).

J.P.Morgan forex forecast updates as well as major investment banks’ forecasts are available to our regular subscribers. Subscribe now or get a free 5-day trial.

CAD Forecast 2021

Near-term headwinds belie solid medium-term outlook

The first quarter of 2021 was stellar for CAD. We have been bullish since January and remain constructive on the currency’s medium-term prospects. April presents some tactical concerns, however, and could moderate but should not derail CAD firmness through the remainder of the year. CAD was the top performer amongst both G10 and EM currencies in 1Q. In our view, this reflects a healthy mix of a solid medium-term local outlook (strong growth, proactive BoC, expected spillover from fiscally-led US growth), complemented by the strong global reflationary backdrop. This was consistent with a dramatic repricing of rates which supported CAD in particular. Over the rest of the year, we continue to believe this mix of factors should underpin CAD performance on a broad basis, albeit it likely at a more moderate pace compared to 1Q. Near-term questions include how the renewed COVID-19 spike impacts the BoC April MPR meeting and whether housing prices are cause for concern, but for now our constructive medium-term outlook remains and we leave our year-end 1.22 forecast unchanged.

CAD remains one of only a couple currencies in G10 where the central bank has signaled steps towards near-term normalization, which should support CAD as peers’ monetary policy remains anchored throughout the rest of the year. The economy continues to outperform expectations into 1Q. The BoC has conditionally tied its tapering to growth performance being “in line or stronger” than their forecasts. That is clearly the case and has thus set a strong expectation among market participants that the BoC will be offering more concrete guidance around its plans, potentially as soon as its MPR meeting in April. A speech by Dep. Gov. Gravelle two weeks ago reaffirmed to us that the BoC is actively preparing for a step down in weekly asset purchases.

The caveat is that the timing and precise strategy around tapering are still up in the air. The recent second wave of COVID-19 in Canada and renewed activity restrictions may force the BoC to adjust its near-term plans, making the April MPR a tactical risk for CAD, given how expectations have been built up for this event. But this should not disrupt the end result that tapering will begin this year. Since peak CAD TWI strength in mid-March, CAD yields have slumped the most in G10 (ex-NZD) in conjunction with rising COVID-19 infections. Ontario has since twice-announced new restrictions for the month of April with the possibility to be longer. The read-through for CAD, in our view, is a tactical one: the BoC meeting falls squarely into this time window, which may make it challenging to reduce accommodation amid another COVID-19 wave. That being said, we do not think this development warrants a wholesale rethink in the growth outlook for Canada, nor the rates market by extension. Canada has demonstrated some resilience to lockdowns based on evidence from Dec-Jan, and vaccinations are gathering momentum. Moreover, the BoC has expressed some discomfort with the size of its footprint in the GoC bond market, which is additional motivation to taper beyond cyclicals. The takeaway is that this is a timing issue for the BoC; they may opt to defer announcing or introducing tapering at the April MPR, but this does not change the ultimate trajectory of tapering ahead of peers, including the Fed.

AUD Forecast 2021

AUD: Sticking to the plan

AUD/USD has drifted lower over the past month, making a new 2021 low just below 0.7550 before moving marginally higher. We have been bearish on the outlook for AUD since mid-2020, largely due to the overt dovishness of the RBA, and while stronger than forecast commodity prices have challenged our forecast, it appears this view is now tracking. We expect the AUD/USD to drift down to 0.71 at Dec-21.

Much of the strength in the exchange rate in late-2020 appeared to be a function of the rally in iron ore, which was underpinned by China’s real GDP recovery on the demand side, and disruptions among major Brazilian producers on the supply side. The correlation between spot iron ore prices and AUD/USD remains tight, with the 7% decline in iron ore since the start of March partly responsible for the directionality of the currency. J.P. Morgan commodity analysts expect iron ore demand to remain robust given strong Chinese steel production. However, with Chinese real GDP growth to moderate back toward pre-COVID run rates it is likely steel production also slows and contributes to a decline in spot prices through 2021. Further, the short beta for iron ore has been lower than its long run average in recent months.

Late last month we recommended selling AUD/USD in cash at 0.7604, with a stop-loss at 0.7788. The motivation for this trade was a combination the RBA’s comparative dovishness vs other CBs, negative carry and already elevated levels of iron ore prices, which in our view made it difficult for AUD to outperform in the anticipated global cyclical upswing. With the Australian data likely to face significant hurdles in the coming months as fiscal stimulus fades (discussed below), we remain committed to this trade and bearish on the near-term AUD outlook.

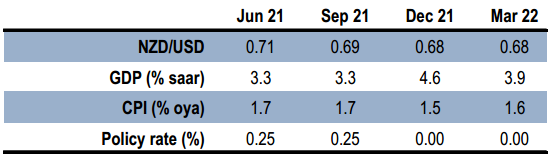

NZD Forecast 2021

Housing end-game in sight, affirming a bearish bias for NZD

NZD/USD is down about 2% since our last Key Currency Views publication, with the primary catalyst being the NZ Government’s surprisingly aggressive housing reforms announced late last month. The richening in local rates was initially quite dramatic out to the belly of the curve (-10bp in NZD 2s/5s/10s IRS), but has retraced more recently. In our view these reforms reinforce, and bring forward the risks to more dovish RBNZ policy that were going to occur anyway due to the central bank’s own macro-prudential tightening. We remain bearish on NZD/USD and forecast 0.68 at Mar-22.

Market expectations for rate hikes built in earlier this year were bootstrapped to a housing upswing that could never have had much longevity. Loan to value ratio (LVR) restrictions were due to be tightened in March and May. The government’s own reforms add a more medium-term drag to housing and credit growth by extending the holding period on capital gains exemption (the “Bright Line” test) from five to ten years, and also remove tax deductibility of interest for investors. This arguably lowers the neutral rate over a longer period.

Both are significant policy changes intended to tilt the balance toward owner-occupiers and particularly, first home buyers (FHBs), at the expense of investors. In combination, these changes also notionally expose potential property investors to the significant curve shape in NZ rates, given the much longer period under which there is no tax shield on interest servicing charges. The government is making these changes precisely because FHBs have traditionally struggled to compete on level terms with investors at current levels of prices and price expectations, even under investor-punitive LVR restrictions. So it is unlikely that rationing investors out will crowd in an equivalent or greater volume of FHBs, without some price concessions. The reforms are therefore likely to see a rotation toward more owner-occupier investor activity, but with weaker medium-term credit and house price growth overall.

Latest research reports from top investment banks are available to our regular subscribers. Subscribe now or get a free 5-day trial.