In this article we are presenting some extracts from investment banks’ research with US dollar predictions 2021, currency market analysis and forecasts for this year, including views from HSBC and J.P.Morgan.

HSBC: USD Outlook: Waiting to board

- The USD has been speeding ahead this year, leading many to question whether they are on the wrong track

- Our train of thought still expects a modest USD decline in the months ahead, as the global economy gains momentum

- Delays are frustrating but a sustained USD recovery is premature

The train is late…

In the previous edition of the Currency Outlook, we discussed how the timing and pace of the USD recovery this year had caught many off guard, including us. Our baseline scenario has rested on the USD facing some modest depreciation pressure amidst the likelihood of a synchronised global recovery. Instead, we have been caught waiting for this train to arrive and increasingly it is running late, as many countries struggle to contain the continued fallout from COVID-19 while the US economy is steaming ahead.

As we have highlighted previously, it makes sense that the delay in global growth synchronisation has played to the USD’s advantage and its resilience has indeed been broad-based, apart from a handful of currencies. However, this is not just a function of the global economy (excluding the US) having lost some momentum compared to a few months ago. The consistent pulling forward of the Fed’s expected rate hike cycle has also added to the USD’s momentum. Given the swiftness of the US economic recovery alongside powerful doses of fiscal loosening, Fed fund futures have nearly discounted the same magnitude of rate increases reached in 2018 (Chart 2). This stands in contrast to many other currencies, in particular the EUR, JPY and CHF with their forward-looking rate expectations largely unchanged.

Yet, this continues to endorse how exchange rates are not solely taking direction from risk appetite, unlike in most of 2020. The train of thought is that economic and short-term interest rate divergence has been playing a bigger role.

Chart 1. USD’s advance continues versus many currencies…

Chart 2. …as Fed rate hikes expectations have been accelerating

On the wrong track?

Although the Fed’s forward guidance has kept the level of short-term interest rates low, the USD has still taken a positive cue from the steepening of short-term US yields. This also shows how the USD’s behaviour has evolved over the past few months, going from a limited relationship late last year to a stronger influence this year (Chart 3). Despite interest rates mattering more, we believe the USD’s inverse relation to risk appetite remains the dominant feature. For the most part, better than expected US data still tends to coincide with a weaker USD via the risk appetite channel rather than a stronger one associated with a stronger US economy. Our USD DRIVERS framework captures this point and is essential to monitor whether it is truly changing behaviour.

Chart 3. Re-pricing the Fed rate hike path has coincided with a USD recovery

Nonetheless, we have to ask ourselves whether we are on the wrong track for the USD since it has performed well this year. We are still not convinced about the timing given some necessary conditions to sustain a USD recovery are missing. This is not just about the USD’s behaviour cited above for a few reasons. First, a steep rate hike cycle is well priced when the Fed only adopted a new framework last August. A stronger USD is not conducive for the Fed to meet its new objective. Second, the bond market may have already discounted a good amount of the coming rise in inflation (Chart 4). Third, we maintain that there is not enough consideration of how currencies perform when US and global growth data strengthened in the past (Chart 5). The USD typically underperforms during such periods and a synchronised growth cycle, albeit an uneven one, should reassert itself more so in the months ahead.

Chart 4. US breakevens have already factored in an increase in core PCE

Chart 5. FX relationships to US and global cyclical upswings

The recovery train elsewhere…

To us, it seems there has been too much focus on the US growth outlook alone rather than considering the global context with an accelerated vaccine rollout. Activity data are improving and the upward surprises in the Eurozone stand out (Chart 6). Despite the continued lockdown measures and slow vaccination progress, the Eurozone’s consumption recovery has been delayed but not derailed. Plus, there would clearly be positive spill-over effects from a strong US economy to elsewhere, which would likely give some support to their respective currencies. It is well recognised that Mexico and Canada’s exports should stand to benefit but others would likely do so too, either directly or indirectly via their supply chains (Chart 7).

Chart 6. Will US growth keep surprising to the upside compared to elsewhere?

Chart 7. Who could benefit from strong US economic spill-overs?

A counter-argument relates to greater US service consumption becoming a meaningful drag to goods’ exporters and their currencies. In our view, this requires some nuanced thinking. The US manufacturing and service sectors tend to grow in a similar direction, as reflected by the ISM surveys. This implies that there is still likely to be healthy demand for goods imports, especially if a US capex recovery continues to unfold. If services spending growth is very strong in the US (as expected), goods spending may still rise, given the enormous spending power of US households in aggregate in 2021. Regardless, the US will not be the sole consumer of goods during a global recovery.

The RMB express paused

A separate but related point comes down to China and the RMB. We referenced how it was first into the crisis and first out last May but this was the reason for us to think that the RMB would not be an outperformer this year. The focus would shift elsewhere as a catch-up story and indeed this has been the case so far for the USD and GBP etc. This is clearly not an exact comparison, as China has been relaxing its outflow channels to moderate RMB appreciation pressure. However, it carries a key message, showing how the focus shifts towards lagging yet improving stories elsewhere rather than sticking with a train that has arrived. We believe the market will soon come to see the USD and GBP in a similar light given their earlier outperformance this year.

A separate issue that we are monitoring is the RMB outlook, which is essential given how it can influence other currencies. The correlation to RMB movements is high for a number of low yielding currencies in Europe and Asia. Our baseline scenario sees the RMB weakening very slightly this year. But the analogies to 2018 are common these days and back then, one reason why the USD was so strong was partly a function of the tariffs rising on China, which caused the RMB and indirectly other currencies to weaken. Should expectations on US-China relations disappoint and as a result the RMB weakens more than we envision, this would be a significant test for our broad USD view. For now, we have pushed back on the idea that the USD can repeat the appreciation path seen in 2018 in the months ahead but the RMB’s role in this context is important.

Conclusion

Our broad message has not changed for some time. We expect some modest USD weakness this year as the global economic recovery gains momentum. The US economy is in the driver’s seat but exceptional growth should only matter for the USD if it drives an exceptional monetary response. The exception this time may be that the Fed sees the outlook differently, with it only willing to change to a hawkish stance if the stronger inflation outlook proves not to be transitory. This probably will not become clear until later this year, so we have months to wait. And the Fed has to wait too, which does not suit impatient USD bulls.

Meanwhile, the market may be starting to realise that the late trains will ultimately arrive at the same station, as the global vaccine efforts pick up. This emboldens the thinking that it will not be the US economy alone that is recovering. Against this backdrop it should steer the USD into a weaker state versus most currencies than has been the case. Even then, however, we believe this should be limited in scale and longevity.

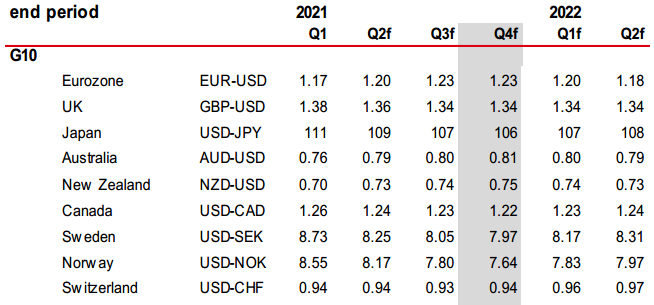

HSBC US Dollar Predictions/Forecasts 2021-22

Forex forecast updates from major investment banks are available to our regular subscribers. Subscribe now or get a free 5-day trial.

J.P.Morgan: USD Outlook: Stuck in the middle

Looking ahead, our narrative on FX and the broad USD remains unchanged. Our expectation has been that the broad dollar index will continue to be pulled in different directions – a fiscal led US exceptionalism which will make higher US yields a recurring issue for markets and is likely to be USD-supportive on the one hand; and a benign global growth environment which should be supportive of selective high beta FX on the other. In our view, USD strength is best positioned for versus currencies where the central bank is likely to remain dovish even as US yields are heading higher (EUR, CHF, JPY). Meanwhile, longs in high beta FX should be selective and funded via EUR, JPY and CHF.

The macro backdrop: higher US yields…

First, an increase in DM yields led by the US is likely to stay a source of support for USD given the combination of outsized fiscal stimulus, strong growth momentum and rising inflation pressures. The growth outlook is improving in most countries but the US has led the way higher given unprecedented fiscal stimulus, which has warranted wider US yield spreads as well (exhibit 1). The fiscal stimulus and the resultant higher Treasury issuance will remain an area of focus for markets. For instance, the US Treasury auctions 3- and 10-year notes on Monday next week; historically such auctions have been subject to weaker demand. Beyond that, phase two of Biden’s infrastructure plan will be unveiled in April with the total now possibly reaching $4tn (in addition to the prior $3tn already announced; see USD). The path to pass these plans will be harder/slower in comparison to the pandemic relief package, but if passed, will be net US growth positive and hence extend the US outperformance narrative further.

Exhibit 1: Higher growth forecasts in the US vs. rest of DM has warranted wider yield spreads in favour of USD

DM growth forecast revision index ex-USD vs. 10y US yield spread to DM (bp)

…better global growth…

Second, growth momentum remains highly positive outside the US as well and should also be supportive of high beta FX performance. The growth momentum was evident in the latest global PMIs which showed that the all-industry PMI surged to a near-seven-year high in March. Our economists note that the underlying details were positive with signals of improvements in the service sector, new orders and employment. The positive is sentiment is echoed similarly in our other metrics. Our economists’ growth forecasts have been upgraded in the past quarter in most regions, even though the largest revisions have come to the US (exhibit 1). And our EASIs are still positive for DM and EM in aggregate (although there are some early signs of EM ex-China losing steam which bears watching; exhibit 2).

Exhibit 2: EASIs are positive outside the US as well

J.P.Morgan economic activity surprise indices

…and higher inflation and oil prices

Finally, inflationary pressures are building as well amid improving growth as is evident in our economists inflation forecast revision indices as well (which are also going up more for the US than for the Euro area and EM; exhibit 3). Better growth also has implications for commodity prices as well, particularly oil (and by extension petro-FX) where our commodity strategists look for demand-side dynamics to push Brent in the mid-$70s this year despite expectations of earlier supply from OPEC+.

Exhibit 3: Inflation forecasts are getting revised up as well

J.P.Morgan inflation growth forecast revision; cumulative change (%pt)

Global FX carry baskets have performed well as US yields increased and global growth was benign

In prior publications, we have highlighted the relative sensitivity of various currencies to US rates and commodity prices via exhibit 4. Commodity FX have historically been more resilient to rising US yields and would benefit from higher commodity prices, as evidenced by their historical betas to both these factors. Meanwhile, JPY and CHF are vulnerable on both dimensions (they have negative betas to both yields and commodity prices/ global growth) if US yields were to continue to head higher. Recent price action illustrates this – high beta FX funded via EUR, JPY and CHF have delivered substantially better risk adjusted returns in the US Treasury sell-off, compared to returns when funded via USD. In addition, global FX carry baskets which have involved being long the highest yielding FX funded through the lowest yielders (EUR, JPY, CHF) delivered positive returns as US yields increased in recent months (exhibit 5).

Exhibit 4: Commodity FX have historically been more resilient to rising US yields and would benefit from higher commodity prices; JPY and CHF are vulnerable on both dimensions

20-year beta of CCY to US yields and commodity prices

Exhibit 5: Global FX carry baskets have delivered positive returns amid higher US yields and benign global growth

Total return index from global FX carry vs. US Treasury yields (%)

Tactical strategy: long USD and selective high beta vs. EUR, JPY and CHF

Specifically, in G10 we have been recommending long USD vs. other reserve currencies like JPY, CHF and EUR where yields are expected to be stickier. We have also been recommending long USD vs. AUD and NZD where the central banks can continue to express a dovish view now that the governments have already tightened/ planning to tighten macro prudential measures to contain housing.

J.P.Morgan US Dollar Predictions/Forecasts 2021-22

Latest research reports from top investment banks are available to our regular subscribers. Subscribe now or get a free 5-day trial.