- Macro: Global growth is likely to moderate further to 3.4% in 2019, with the slowdown set to intensify in 2020 as the US slips into a mild recession. The Fed will probably hike rates through 1H19 and reverse course in 2020 with three cuts. The ECB will have just enough time to exit negative rates in 1Q20 before eurozone growth weakens materially.

- FI: We expect 10Y US yields to peak in the 3.25-3.50% range in mid-2019 before falling back to 2.75% by year end, with the curve inverting. Pressure on core EGBs is likely to be limited. We expect BTP spreads to widen to 350-375bp in 1H19 due to high supply and political uncertainty, before easing back to 275bp later in the year.

- FX: EUR-USD is likely to slip to 1.08 by mid-2019, reflecting the risk picture and the US-eurozone growth differential. A reversal back to 1.20 seems likely in 2020 as the Fed starts cutting rates. Sterling has room to rebound once Brexit-related uncertainty recedes. The JPY and the CHF will likely rise over a two-year horizon.

- Equities: We expect 2019 to be a volatile – and mostly unattractive – year for equities. Our 2019 year-end index target for the Euro STOXX 50 is 3300, for the DAX 12000 and for the FTSE MIB 19800. 2019 will be dominated by a slowdown in earnings growth globally. We still consider consensus estimates to be too optimistic.

- Credit: Investors should prepare for considerable spread widening in 2019 as there will be a slowdown in earnings alongside an economic deceleration. Credit fundamentals of European corporates are in better shape than those of US peers and a decline in issuance activity will partly offset the substantially reduced demand from the CSPP.

- CEEMEA: EMFX should continue to perform poorly in trade-weighted terms given the deteriorating trend in global trade volumes, but EMFX-USD could get a lift along with EUR-USD in 2H19. EM credit will likely face pressure in 1H19 but some relief should be seen in 2H19 as the dollar eases and US yields come down.

FX Strategy: For EUR-USD, things will get worse before they get better

- Our fair value projections suggest that the deterioration in fundamentals that has driven EUR-USD lower this year will likely continue in 1H19. In combination with the risk picture, we expect this to trigger further euro selling, taking EUR-USD to 1.08 by mid-2019. From 3Q19 onwards, we expect EUR-USD to recover on the back of more-supportive fundamentals, although spillover effects of the global downturn on the eurozone will likely limit the pullback in EUR-USD to 1.20 by the end of 2020.

- Sterling is set to recover somewhat once the Brexit risk premium is reduced. The JPY and the CHF will likely appreciate, reflecting the global risk picture and the economic backdrop.

Fundamental backdrop has deteriorated for EUR-USD…

Weakening fundamentals and the global risk picture, dominated by the US trade conflict, have put downward pressure on EUR-USD in 2018. Following the latest update of our fair valuation framework, BEER by UniCredit (see Box 1), our estimates show a decline in the fair value of EUR-USD from a peak at 1.23 in 2Q16 to a current estimate of 1.15 (Chart 1; Table 1). The deterioration of the fair value of EUR-USD has largely been driven by interest rate differentials, which have moved strongly in favor of the US, and smaller changes in inflation differentials, terms of trade and investment as a percentage of GDP.

…but this is likely to reverse from mid-2019 onwards

From a long-term perspective, we expect this development to reverse. US-EU yield differentials are likely to tighten from mid-2019 onwards (see FI section), and investment as a percentage of GDP will likely fall in the US while remaining stable in the eurozone. This should more than offset the negative effect on the fair value of EUR-USD resulting from CPI inflation falling more rapidly in the US than in the eurozone. Conditioning on the path of macro variables that we expect over the next couple of years, we project that the fair value of EURUSD will rise to around 1.21 in 2020. This suggests that while fundamentals are unlikely to support EUR-USD in the near term (we think they may actually still worsen somewhat over the next couple of quarters), the longer-term prospects look much brighter.

Considering a range of short-term model estimates for guidance on short-to-medium term developments, we find that EUR-USD is approximately fairly valued at current levels (Chart 2). Based on its past relationship with US-EU real swap rate differentials, there is still some room to the downside, especially if we see a further widening of the differential in 1H19.

EUR-USD to drop to 1.08 in 1H19…

Against this backdrop, the next couple of quarters will likely remain challenging for EUR-USD. In addition to economic developments in the US, which we continue to expect to support two more Fed hikes in 2019 while the policy normalization in the eurozone will remain very gradual (leading to a widening of US-EU interest rate differentials at the short end of the curve), the risk picture suggests that headline risk in the eurozone will remain high in 1H19. Therefore, we think EUR-USD is likely to weaken before it gets stronger. We expect the exchange rate to fall to 1.08 in 2Q19.

…before rising to 1.20 by 2020

However, this is set to change as economic data from the US become more mixed in 2H19 and signals of an imminent downturn in the US start to mount. When the Fed reaches the end of its hiking cycle and the ECB gradually lifts the depo rate back to 0%, which we expect to occur between 3Q19 and 1Q20, fundamentals will turn euro-supportive. This will become even more pronounced when the Fed starts cutting rates, which we see happening from 2Q20 onwards, given that the slowdown in the US will likely be sharper and more pronounced than in the eurozone. By the end of 2020, we expect EUR-USD to have risen to 1.20.

Source: Bloomberg, UniCredit 2019 Market Outlook

You can receive 2019 Market Outlook from major investment banks directly to your Inbox. Subscribe now or get a free 5-day trial.

Sterling to appreciate on the back of a Brexit deal

The question of whether a withdrawal agreement between the UK and the EU can be reached and ratified remains the most important driver for sterling over the coming months and will heavily influence the currency path over our forecast horizon.

As discussed in the UK section, our base case scenario remains that reason will prevail and the UK will leave the EU in March 2019 (or slightly later) with a deal that allows the country to keep close ties to the EU. The resulting reduction of uncertainty should allow the GBP to appreciate considerably, although the risk premium is unlikely to disappear completely, given that uncertainty will still be higher than it would have been had the UK remained in the EU (Chart 3). At the same time, the weaker EUR-USD that we expect in 1H19 will likely take its toll on EUR-GBP. Accordingly, we see EUR-GBP dropping to 0.83 in 1Q18, followed by a further decline to 0.80 in 2Q19.

During 2H19, spillover effects from the expected slowdown in the US are likely to pose a new challenge to the UK economy. This will likely keep EUR-GBP in the 0.81-0.82 range for a few quarters, although GBP-USD may still see some upside during this time as we expect the degree of the slowdown in the UK to be somewhere between the US and the eurozone. We expect a gradual rise in cable from 1.33 in 1Q19 to 1.40 in 4Q19, followed by a stable development in 1H20.

In mid-2020, pressure on sterling is likely to re-emerge. First, the BoE will likely follow the Fed in cutting rates. Second, the UK faces the risk of a new cliff-edge in 2021, as the expected withdrawal agreement would run out on 31 December 2020, and we see it as likely that clarity on any subsequent arrangement will only be achieved at the last minute. If this year’s pattern is repeated, investor nervousness about a potential cliff-edge will peak in the summer, when we could see EUR-GBP rising back to 0.85 in 3Q20. Later in the year, confidence in a deal may increase, which is why we predict EUR-GBP at 0.84 in 4Q20. Accordingly, we would expect cable to fall back below 1.39 in 3Q20, followed by a strong recovery to 1.43, as the result of USD weakening and under the assumption that uncertainty is reduced towards the end of 2020.

No-deal Brexit the biggest risk to our view on the GBP

The biggest risk to our view on sterling is a no-deal Brexit. As pointed out above, we share the market’s optimistic take on the probability of a deal and expect the GBP to appreciate on the back of this outcome. That said, the risk of a no-deal Brexit is non-negligible and would likely cause another episode of sharp sterling depreciation. We would see risks of EUR-GBP breaking above 0.95 in the near term.

The market has finally started pricing in higher Brexit risks when it comes to implied volatility for EUR-GBP. As discussed in FX Perspectives – “Deal or no deal? Assessing the Brexit risk premium in GBP spot and options markets”, until recently, market pricing looked benign compared to prior episodes of UK idiosyncratic risk (Chart 4). Given that decisions with a major market impact will likely be made over the coming weeks and months, we think implied volatility will likely remain at elevated levels until there is more clarity on Brexit.

Source: Bloomberg, UniCredit 2019 Market Outlook

JPY on a recovery path notwithstanding the BoJ’s brake

Two factors are expected to remain the major drivers for the JPY next year and in 2020: swings in global risk aversion and whether the BoJ intends to continue its ultra-loose monetary policy. In turn, last summer’s experience has been quite revealing as to the role the Japanese unit is likely to assume as a safe-haven currency. In particular, the collapse of the TRY in August failed to spark the usual “flight to quality” in favor of the JPY, while the CHF appeared to resume a more active role after having decoupled from risk for years.

However, this apparent change in global investor preference for safe-haven currencies, which we discussed in our FX Perspectives – ‘Stairway to (safe) havens’: reshuffling the rank of favored currencies was largely reversed in the Autumn, when escalating tensions across equity market spilling from the US to the rest of the world induced renewed JPY purchases.

This reaction suggests that at present the JPY probably needs an abrupt spike in global risk aversion, as captured by the VIX index (Chart 5), to attract market interest and resume a more preeminent role as a safe-haven currency. Otherwise, USD-JPY will likely tend to remain stuck in the 110/115 band, as it happened in the past months. We think that the BoJ’s unwillingness to change its ultra-loose monetary policy anytime soon has played a key role in preventing a sustained JPY appreciation during this period of rising interest rates worldwide. This is particularly evident for USD-JPY, as the comparison with the 10Y yield spread between the US and Japan shows in Chart 6.

Nevertheless, there is a possibility that the BoJ may eventually consider some adjustments in its monetary policy strategy over the next two years, although at the October meeting BoJ Governor Haruiko Kuroda made it clear again that the board was in no rush to normalize its policy. The BoJ again downgraded its inflation outlook and also admitted an increase in downside risks for Japan. Looking ahead, a brighter economic picture, and, more critically, inflation re-approaching the 2% target also on the back of the sales tax hike from 8% to 10% in October 2019, remain two pre-conditions for the BoJ to make its monetary strategy less accommodative than it is now.

Hence, assuming at least some BoJ adjustments on the policy front, such as removing the current 0.10% cap on the 10Y yield, we would still expect USD-JPY to weaken over the next two years, albeit gradually. We expect the pair to drop to 103 at the end of our forecasting horizon, while EUR-JPY is likely to slide and then steady at the lower end of the 120-125 range. In both cases, at the end of 2020, the JPY would remain somewhat undervalued with respect to our fair value estimate of 103 for USD-JPY and 118 for EUR-JPY.

Source: Bloomberg, UniCredit 2019 Market Outlook

CHF to strengthen on European jitters in 2019; easing its grip in 2020

As mentioned before, the CHF had apparently resumed its role of a safe-haven currency in the summer, but it rapidly lost its ability to hold gains in the Autumn, as shown in Chart 7. The rapid reversal that pushed USD-CHF back to parity after the August fall below 0.96 amid the TRY crisis and growing political tensions in Italy, was probably due to the renewed broadbased USD appreciation.

We still expect the CHF to be the main catalyst for pressure that may further affect Europe in the coming months. Its additional strengthening is set to remain under the SNB’s control, but Swiss fundamentals do justify more currency strength this time: we estimate EUR-CHF fair value at around 1.10 (Chart 8), and the SNB may thus ultimately prove more relaxed on the currency front over the coming quarters. Therefore, a brief undershooting down to 1.08, could be possible in the course of 2019.

External issues may keep the Swiss franc firm next year, but its underlying strength is set to remain in place throughout our entire two-year forecast horizon, given the overall risk picture and the downturn we expect in the US and the eurozone. For 2020 we only see a modest EUR-CHF pick-up to around 1.12, which remains well below the past reference threshold for the SNB of 1.20 that was nearly tested in April.

Source: Bloomberg, UniCredit 2019 Market Outlook

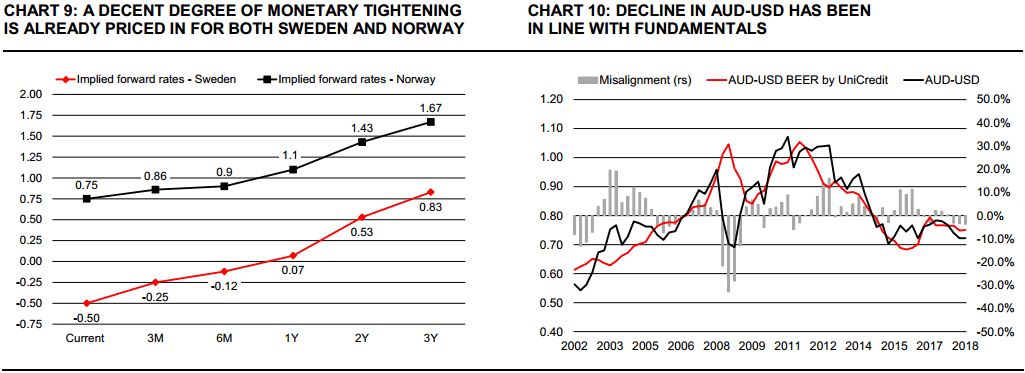

Higher SEK and NOK ahead, but monetary tightening at home is largely priced-in

In the course of 2019 and 2020, the two Nordic currencies have to deal with the progressive normalization of their central banks’ monetary policies. The Riksbank will likely start and the Norges Bank already hiked the deposit rate in September and is set to continue. Still, there are two drags in this apparently very favorable scenario for the SEK and the NOK.

First, the Swedish housing market remains fragile, which may make the Riksbank prudent in its pace of tightening. Second, a decent degree of tightening is already priced in by the two forward curves: over a 2Y horizon, they are incorporating roughly a 100bp rate hike in Sweden and nearly 70bp in Norway, as shown in Chart 9.

We remain convinced that these two currencies will be stronger in two years’ time. However, their rally is unlikely to be as impressive as their still huge undervaluation may suggest, unless, of course, both central banks surprise investors on the hawkish side, a prospect that seems rather unlikely in our view. In the meantime, other external factors – world trade, global risk considerations and the retreat of oil prices that we consider in our outlook – may act as a further brake along the appreciation road for the SEK and the NOK.

Source: Bloomberg, UniCredit 2019 Market Outlook

Commodity currencies likely to see further pressure as the global economy slows

Commodity currencies have suffered from rising concern about the effect of US trade tension on global growth this year – and our economic outlook suggests they may not be out of the woods yet.

Based on our BEER model, this year’s depreciation of the AUD, the NZD and the CAD has been fully backed by a deterioration in fundamentals (Chart 10). In particular, developments in commodity prices have led to an unfavorable development in the countries’ terms of trade, and a reduction of expectations for monetary policy tightening in the Pacific Rim. This is likely to continue, as slower global growth from 2H19 is likely to put further pressure on commodity prices from the demand side (see Oil section).

Over a two-year time horizon, market-implied policy rates for the Reserve Bank of Australia (RBA) and the Reserve Bank of New Zealand (RBNZ) are currently about flat, while the market is prepared for three rate hikes by the Bank of Canada (BoC). We agree with this assessment as far as 2019 is concerned. However, if the Fed cuts rates in 2H20, past experience strongly suggests that central banks in Australia, New Zealand and Canada will follow.

In our view, this makes all three commodity currencies prone to further weakness over the next couple of years. By the end of 2020, we expect the AUD and the NZD to have dropped close to 10% against the USD, with our end-2020 forecasts for AUD-USD at 0.65 and for NZD-USD at 0.61. For the CAD, the depreciation may be alleviated by the fact that the currency is already trading considerably below its fair value. We therefore expect USD-CAD to remain relatively stable over the course of 2019 but expect the CAD to weaken against the USD in 2020, when we expect USD-CAD to reach 1.35.

Challenges for EM FX to remain in place

For EM FX, we are likely to get EMFX-USD crosses tracking the EUR-USD move lower in 1H19 before gently moving higher in 2H19. However, we do not see the ingredients for a recovery in EMFX in trade-weighted terms. In contrast, we believe further weakness is in store in 1Q19. For USD-CNY, we pencil in a gradual rise to 7.12 by the end of 2019.

You can receive 2019 Market Outlook from top investment banks (e.g. Giti, Goldman Sachs, Morgan Stanley, HSBC, UBS) directly to your Inbox. Subscribe now or get a free 5-day trial.