If you wish to receive this Societe Generale research report (and many other) on a daily basis, subscribe now or get a free 5-day trial.

Forex Trade Idea – Go long AUD/USD vol against USD/JPY vol (Societe Generale Research)

Rationale: Low and cheap volatility spread

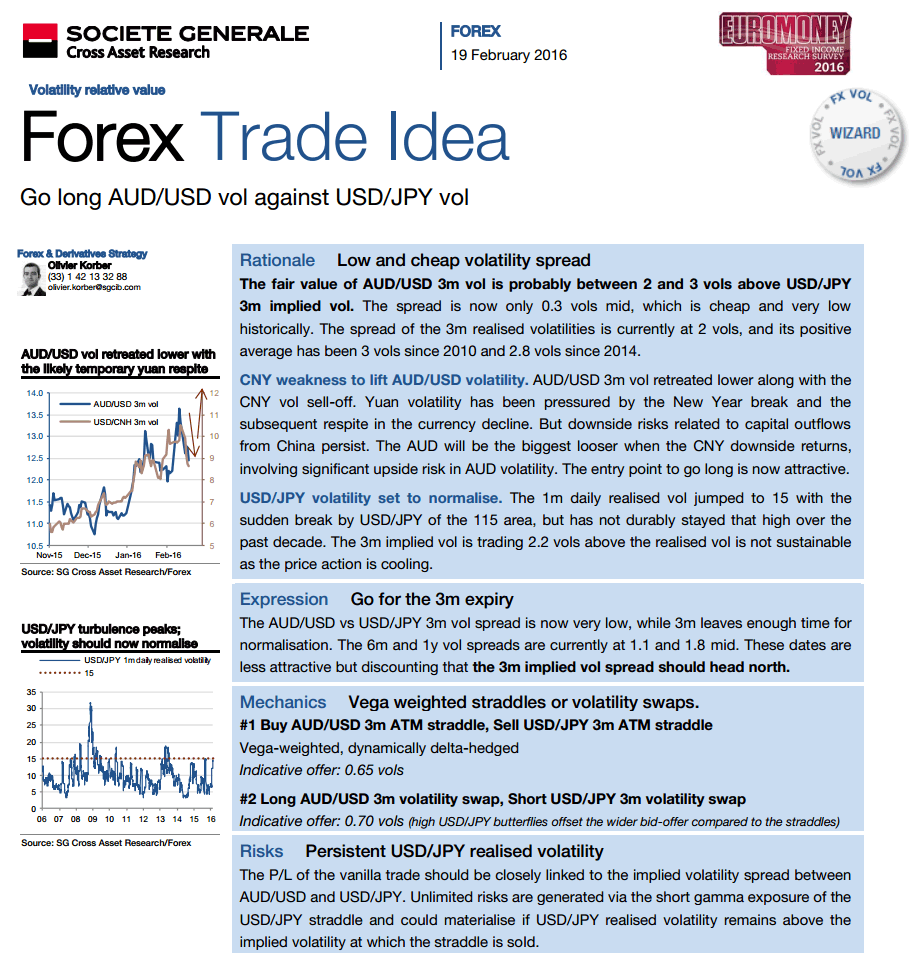

The fair value of AUD/USD 3m vol is probably between 2 and 3 vols above USD/JPY 3m implied vol. The spread is now only 0.3 vols mid, which is cheap and very low historically. The spread of the 3m realised volatilities is currently at 2 vols, and its positive average has been 3 vols since 2010 and 2.8 vols since 2014.

CNY weakness to lift AUD/USD volatility. AUD/USD 3m vol retreated lower along with the CNY vol sell-off. Yuan volatility has been pressured by the New Year break and the subsequent respite in the currency decline. But downside risks related to capital outflows from China persist. The AUD will be the biggest looser when the CNY downside returns, involving significant upside risk in AUD volatility. The entry point to go long is now attractive.

USD/JPY volatility set to normalise. The 1m daily realised vol jumped to 15 with the sudden break by USD/JPY of the 115 area, but has not durably stayed that high over the past decade. The 3m implied vol is trading 2.2 vols above the realised vol is not sustainable as the price action is cooling.

Expression: Go for the 3m expiry

The AUD/USD vs USD/JPY 3m vol spread is now very low, while 3m leaves enough time for normalisation. The 6m and 1y vol spreads are currently at 1.1 and 1.8 mid. These dates are less attractive but discounting that the 3m implied vol spread should head north.

Mechanics: Vega weighted straddles or volatility swaps

#1 Buy AUD/USD 3m ATM straddle, Sell USD/JPY 3m ATM straddle

Vega-weighted, dynamically delta-hedged

Indicative offer: 0.65 vols

#2 Long AUD/USD 3m volatility swap, Short USD/JPY 3m volatility swap

Indicative offer: 0.70 vols (high USD/JPY butterflies offset the wider bid-offer compared to the straddles)

Risks: Persistent USD/JPY realised volatility

The P/L of the vanilla trade should be closely linked to the implied volatility spread between AUD/USD and USD/JPY. Unlimited risks are generated via the short gamma exposure of the USD/JPY straddle and could materialise if USD/JPY realised volatility remains above the implied volatility at which the straddle is sold.

You can find more Societe Generale research reports as well as other analysis from well-known institutions via our subscription.