If you wish to receive BNP Paribas Forex Weekly Strategy pdf analysis (and many other research reports) on a regular basis, subscribe now or get a free 5-day trial.

Forex Weekly Strategy: GBP squeeze could be coming to an end

- STEER™ signals the GBP is expensive and expectations for further Bank of England easing have now mostly unwound.

- Our economists still expect a Federal Reserve hike in September. We remain broadly bullish on the USD.

- The market has interpreted recent Bank of Japan comments as reducing the likelihood of 21 September easing.

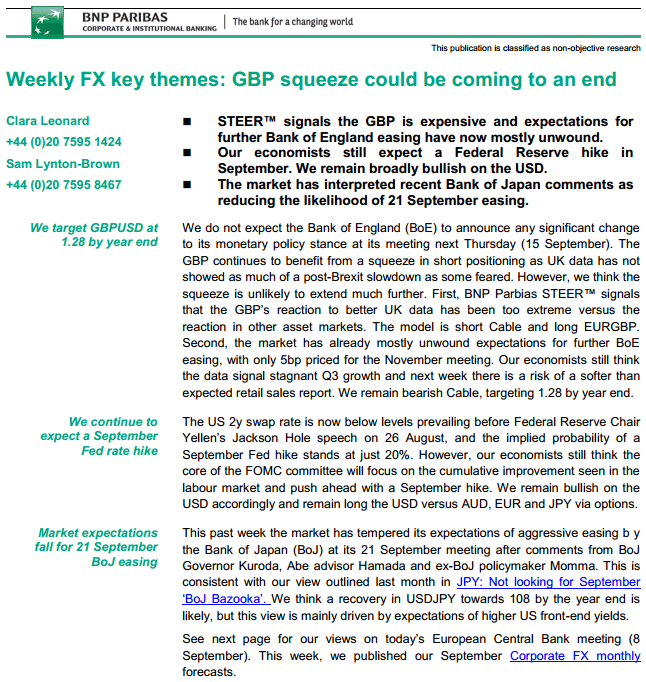

We do not expect the Bank of England (BoE) to announce any significant change to its monetary policy stance at its meeting next Thursday (15 September). The GBP continues to benefit from a squeeze in short positioning as UK data has not showed as much of a post-Brexit slowdown as some feared. However, we think the squeeze is unlikely to extend much further. First, BNP Parbias STEER™ signals that the GBP’s reaction to better UK data has been too extreme versus the reaction in other asset markets. The model is short Cable and long EURGBP. Second, the market has already mostly unwound expectations for further BoE easing, with only 5bp priced for the November meeting. Our economists still think the data signal stagnant Q3 growth and next week there is a risk of a softer than expected retail sales report. We remain bearish Cable, targeting 1.28 by year end.

The US 2yswap rate is now below levels prevailing before Federal Reserve Chair Yellen’s Jackson Hole speech on 26 August, and the implied probability of a September Fed hike stands at just 20%. However, our economists still think the core of the FOMC committee will focus on the cumulative improvement seen in the labour market and push ahead with a September hike. We remain bullish on the USD accordingly and remain long the USD versus AUD, EUR and JPY via options.

BNP Paribas Forex Weekly Strategy pdf reports are available to our subscribers.

Subscribe now or get a free 5-day trial.

This past week the market has tempered its expectations of aggressive easing by the Bank of Japan (BoJ) at its 21 September meeting after comments from BoJ Governor Kuroda, Abe advisor Hamada and ex-BoJ policymaker Momma. This is consistent with our view outlined last month in JPY: Not looking for September ‘BoJ Bazooka’. We think a recovery in USDJPY towards 108 by the year end is likely, but this view is mainly driven by expectations of higher US front -end yields.

EUR: ECB passes baton to the Fed

- The market only held a light EUR short position heading into the European Central Bank (ECB) meeting.

- After the ECB kept policy unchanged, the focus now shifts firmly to the US Federal Reserve.

- We remain bearish on EURUSD; we target 1.08 by the year end.

The ECB refrained from announcing new easing measures at today’s monetary policy meeting. President Mario Draghi stated in the press conference that the central bank did not discuss an extension of the current asset purchase programme. He stressed that risks to economic growth lie to the downside but that, for the time being, changes to the ECB’s growth and inflation forecasts are not large enough to warrant more easing. However, our economists view today’s decision as a postponement rather than a rejection of further easing with new announcements likely soon, most probably at the December ECB meeting after a full evaluation of the options available.

BNP Paribas Forex Weekly Strategy pdf reports are available to our subscribers.

Subscribe now or get a free 5-day trial.

The EUR initially benefitted modestly from the ECB’s decision to leave policy unchanged with EURUSD rising from 1.1290 before the announcement to a high of 1.1328. Given that short EUR positioning is quite light, at -8 in the range of -50 to +50 according to BNP Paribas FX Positioning Analysis, we would not expect the EUR’s squeeze upward to extend on the topside and be sustained.

The ECB has passed the baton to the US Federal Reserve in terms of determining EURUSD’s direction. Overall, disappointment at the lack of an ECB policy adjustment has only been worth about 2bp on the EUR 2y swap rate. Hawkish comments from key members of the US Federal Reserve ahead of next Tuesday’s start to the comment blackout period could easily move US front-end yields by several times that amount very quickly.

We continue to forecast a fall in EURUSD to 1.08 by the end of the year, consistent with our economists’ view that the Fed is likely to raise US rates by 25bp at the 21 September meeting (versus market pricing in of only a 20% probability of such a rate hike). We remain short EURUSD via a ratio put spread with KI: buy 1x 1.09, sell 2x 1.05 with a 1.0250 KI (30 September 2016 expiry).

G10 central banks at rest?

- Markets are pricing very little from G10 central banks for the final four months of the year.

- We think the market is underpricing BOE easing, overpricing BOJ easing, and underpricing Fed hikes.

- Market positioning suggests relative value trades should focus on GBPUSD.

Investors have returned from their summer holidays to a market priced for virtually no G10 central bank action before the end of the year. As Chart 1 below shows, markets are currently not fully priced for policy change from any of the G10 central banks in the coming four months other than the Bank of Japan. If market pricing proves correct, this would represent a different end to the year than we experienced in 2015, when the Federal Reserve hiked, and the ECB, the RBNZ and Norges Bank all eased. FX option pricing is arguably consistent with the subdued outlook, with a DXY-weighted measure of 3m volatility now at 8.8% vs. closer to 11% at the beginning of September 2015.

The lack of action expected by the financial markets reflects two primary assumptions. First, markets believe the Fed will be unwilling and unable to proceed with rate hikes over the next few months. Second, a perception exists that most other G10 central banks have exhausted most of their ammunition with respect to conventional policy easing, and thus are not likely to cut rates much further.

BNP Paribas Forex Weekly Strategy pdf reports are available to our subscribers.

Subscribe now or get a free 5-day trial.

We agree primarily with market pricing for limited policy action from G10 central banks in the final months of the year. The table below compares our views with the current market pricing. Indeed, we think the rates markets may even be overpricing scope for the Bank of Japan to push cash rates lower, with the Bank of Japan more likely to focus on adjustments to its asset purchase program than rates policy at the September meeting.

Our main disagreements with market pricing as we head into the final months of the year relate to pricing for the Fed and Bank of England, with the former still likely to hike rates, in our view, and the latter expected to cut rates further.

Accordingly, we are now most focused on the USD and GBP for relative value opportunities.

Rates markets have been persistently unwilling to increase pricing for Fed hikes since June, despite a fairly steady stream of hawkish comments from officials and strong labour market data. Our economics team continues to expect a rate hike in September, implying an adjustment higher in Fed pricing is likely in the weeks ahead.

The Bank of England has had a run of upside surprises on key releases for August, and, as a result, the markets have scaled back expectations for further easing. Our economists expect data to be less robust going forward and still believes as its base-case scenario that the Bank is likely to deliver a further 15bp of rate cuts in November.

BNP Paribas Forex Weekly Strategy pdf reports are available to our subscribers.

Subscribe now or get a free 5-day trial.

Market positioning has adjusted to reflect the shift in rate hike expectations for the BOE and the Fed, with cable short positioning recovering sharply from an extreme short position in July to only a modestly short position now. The short covering process could have further to run in the near term, but the lightening of positions should ultimately create opportunities for shorts. Short GBPUSD is likely to be an attractive trade again as we move into autumn.

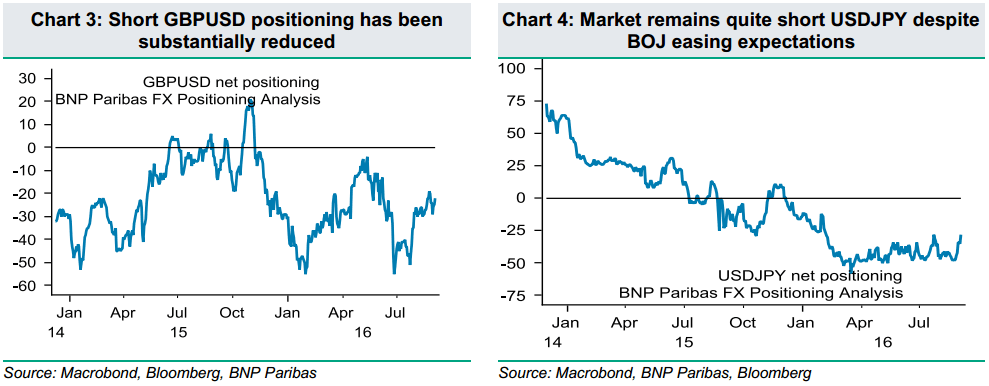

Our view that Bank of Japan (BOJ) policy easing will likely fall short of expectations might suggest opportunities to go long yen in the months ahead. However, our position metrics suggest that, despite rate markets pricing additional BOJ action, currency market participants have actually been positioned long yen, apparently sceptical that further BOJ easing would succeed in weakening the currency. For USDJPY, we think a market shift to price further Fed action would dominate any impact of disappointment with respect to BOJ action. We remain bullish USDJPY accordingly.

You can get BNP Paribas Forex Weekly Strategy research reports as well as many other analytics from tier 1 institutions via our subscription.