If you wish to receive Barclays trade of the week as well as many other research from major institutions on a regular basis, subscribe now or get a free 5-day trial.

FX Thoughts for the Week Ahead – US election debate in focus

• The USD will likely trade sideways after losing some ground since the FOMC decision last week. Market expectations for a December hike barely changed, with markets pricing a 55% chance of a hike, although the “dots” only point to two hikes instead of three during 2017. Incoming data should help to confirm this view, although we think that the status quo in terms of inflation and unemployment is sufficient to warrant a hike before year-end.

• Market attention will shift to US politics as the first US presidential debate takes place on Monday. Recent outperformance of Trump in the polls has materially tightened the race, increasing the uncertainty regarding the potential outcome and affecting some currencies that would be clearly impacted by his anti-immigration and anti-trade rhetoric. In this regard, we anticipate increasing market sensitivity to the potential outcome of the presidential race as we approach critical dates.

• High yield and high beta assets should perform well except for those tightly linked to the outcome of the US election as volatility has receded from its temporary spike.

• Data wise the calendar is relatively light. China Caixin manufacturing and official PMIs take centre stage. US PCE, EZ inflation and UK service index are the main economic releases in developed markets.

• In the Central Bank space, Mexico, Colombia, Taiwan, Czech Republic and Israel will make monetary policy decisions. We expect all of them to stay put although Banxico is a tight call as MXN has continued underperforming its peers materially.

• Trade for the week ahead: Sell 3m 25d RR in USDMXN (delta hedged)

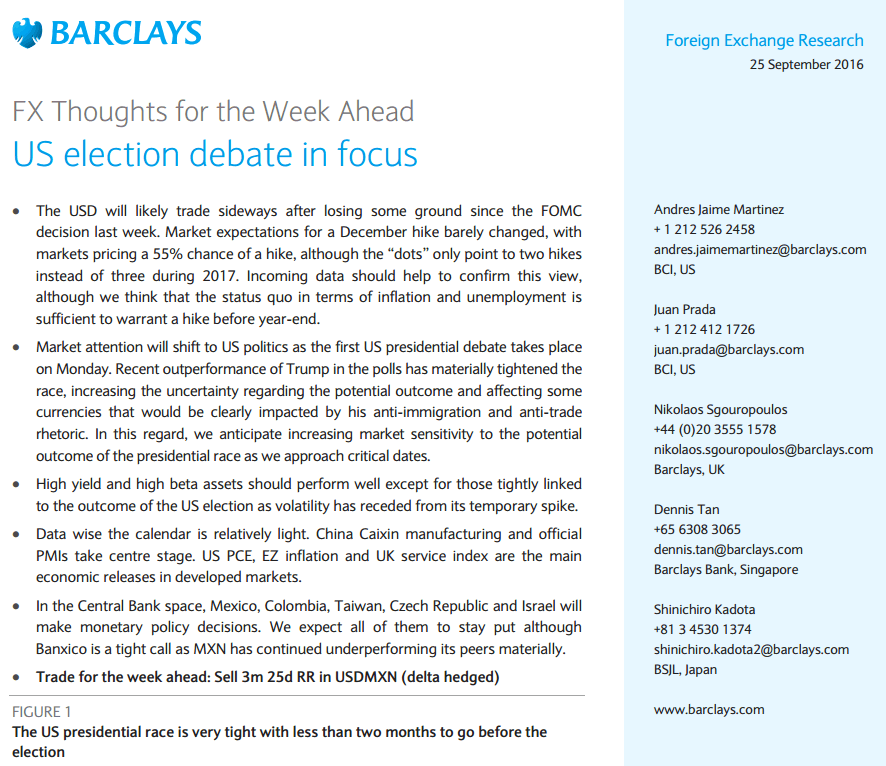

FIGURE 1

The US presidential race is very tight with less than two months to go before the election

Overview: US election debate in focus

The USD will likely trade sideways after losing some ground since the FOMC decision last week. Despite not hiking interest rates in its September meeting, the FOMC signalled its intentions to increase at least once before year-end. Therefore, market expectations for a December hike barely changed and remain above 50%. We do think that markets will continue to price a higher probability as we approach year-end due to the fact that the status quo in terms of inflation and labour market dynamics should be sufficient to support an increase in fed funds rate before year-end.

Barclays Trade of the Week and other trade ideas from top investment banks are available to our subscribers. Subscribe now or get a free 5-day trial.

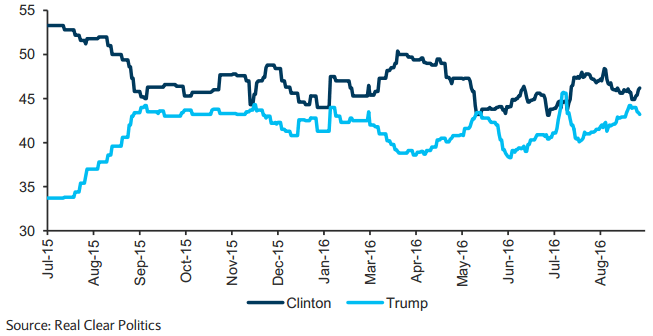

More important will be the first (out of three) US presidential debates on Monday. As the race between Hillary Clinton and Donald Trump has tightened and we approach November 8, we expect a tighter correlation between the financial asset prices and the subjective assessment of the outcome of the elections (Figure 2). The higher percentage of undecided voters (around 20%) compared to four years ago (12%) increases the relevance of the debates as they could shift the odds in either direction.

High yield and high beta assets should perform well except for those tightly linked to the outcome of the US election as volatility has receded from its temporary spike. The Fed’s decision to remain on hold and BoJ’s guidance regarding monetary policy helped to calm down recent concerns about a drastic increase in yields in core markets. Therefore, the resent sell-off in long-term bonds in core markets receded, helping to cap the recent increase in volatility. On the other hand, we would not expect to see a substantial decline in volatility in assets tightly linked to the US election outcome such as MXN, CAD and some Asian currencies.

The main economic release this week will be PMI data in China and inflation figures in the US (PCE) and Europe. In addition, no major central banks are scheduled to meet this week. In the emerging market space, Mexico, Colombia, Taiwan, Czech Republic and Israel will hold monetary policy decisions. Mexico stands out as a close call given the recent underperformance of MXN mainly related to politics in the US.

FIGURE 2

Correlation with the implied probability of Trump winning the presidential election

Trade of the week: Sell 3m 25d RR in USDMXN (delta hedged)

Although USDMXN tends to trade with an upside skew, in the past few days, the market has been clearly biased to the upside. Despite the undervaluation of MXN, the skew continues to widen (Figure 3). In addition, the “realized” skew has increased substantially, even adjusted by what is implied in the options market. In addition, market nervousness about the US presidential elections has increased USDMXN speculative activity, driving 3m risk reversals relative to some of its peers to levels not reached in the past ten years (Figure 4).

While the FX commission acknowledges that capping the level of USDMXN is impossible and not desirable, it might want to lower the incentives of using MXN as a one-way trade, and it could take advantage of the short positioning of the market by intervening in a discretionary basis in USDMXN, something that will likely reduce the implied skew.

This trade recommendation (trade of the week) is valid from the Wellington open Monday morning to the New York close Friday. Last week’s recommended Trade for the Week Ahead no longer is valid.

You can get Barclays Trade of the Week and many other institutional strategies via our subscription.