HSBC Currency Outlook reports are available to our regular subscribers. Subscribe now to access institutional research reports or get a free 5-day trial here.

HSBC Currency Outlook

GBP: Weakness to remain

- The Conservatives have hung onto power, but failed to secure a majority in the House of Commons

- This could complicate Brexit negotiations as Theresa May has not achieved the mandate she sought

- Instability looms: the domestic policy agenda will be constrained, we retain our GBP-USD forecast of 1.20 for year-end

The Conservative party is set to form a minority government, after suffering losses at the UK general election on 8 June. A minority Tory government was almost unthinkable when Theresa May called the snap election and GBP has already come under significant pressure in the aftermath of this surprising result (Chart 1). The election was supposed to clear up political uncertainty, but instead has added another layer of uncertainty to GBP’s outlook. We believe another bout of GBP weakness lies around the corner as the market considers a combination of domestic and external political volatility.

1. Cable responds to domestic politics

Source: HSBC Currency Outlook, Bloomberg

Domestically, the Conservatives could struggle to deliver on their manifesto promises. The Conservative Party is currently looking at some form of arrangement with Northern Ireland’s Democratic Unionist Party in order to generate a tiny working majority on key issues. Yet such agreements tend to be weak and difficult to maintain. In the post-war era the UK has seen three minority governments, all of which have struggled to hold onto power. The last minority government occurred under John Major in late 1996, following a string of by-election losses and defections. Having initially held a small majority after the 1992 general election, Major’s minority Conservative government struggled to pass any significant legislation. There is much uncertainty surrounding Prime Minister May’s leadership. Although she had stated she will continue as PM, if her position comes under threat from her own party due to this poor showing, it will only add to the political uncertainty prevailing, putting further downward pressure on GBP.

The minority government will still have to navigate the UK out of the European Union. Significant legislation in the form of the Great Repeal Bill – a key step in leaving the EU – may still make it through parliament. Brexit will become the single focal point for this government. The market will try to understand whether this election result is partly a vote against a “hard Brexit” and whether the negotiations will take on a softer stance from the UK side. On several occasions, Theresa May has reiterated that “no deal is better than a bad deal”. The potential cliff-edge of a “no deal” is still there – a line of thinking that particularly worries the pound. The clock is already ticking towards the March 2019 deadline, as set out by the Article 50 timetable. The tone of the forthcoming negotiations will be a determining factor in how GBP performs in the coming months. Sticking to the “no deal” mantra would be damaging for GBP.

Structural and cyclical drivers add to the Brexit uncertainty for GBP. The still wide trade deficit remains a recurring headache that likely requires a further adjustment lower in GBP. Cyclically, there are some signs that economic momentum is losing traction (Chart 2), notably through slower consumer spending that has driven GDP growth lower.

2. UK Surprise Index chart

Source: HSBC Currency Outlook, Bloomberg

We believe that GBP will resume its weakening path given the combination of these political, structural and cyclical factors. A renewed focus on the possibility of a “no deal” scenario will likely see Cable revisit 1.20 by the end of 2017. If the EUR continues on its upward path, as we expect, then GBP weakness would be even more pronounced against the EUR. The election may be over but the politics has just begun.

Another Conservative-led government is in store

The election results indicate the Conservatives should retain power, but without a majority and possibly supported by an alliance with Northern Irish unionists. In a major turnaround from the start of the election campaign (where polls were pointing to a majority of over 100) the Conservatives lost 13 seats, leaving them short of an outright majority. On the other hand Labour gained 30 seats. The Lib Dems made gains, while the Scottish National Party (SNP) lost more than 20 seats, making a second independence referendum less likely.

Given the credibility hit Mrs May has taken, we would not rule out her standing down, or facing a leadership challenge.

A wider range of Brexit outcomes is now possible

The election offered voters a choice between two very different visions: a high tax and spend economy with the door open to a softer Brexit, or a continuation of fiscal consolidation and the ‘hard’ Brexit outlined by Theresa May. In the end, the country looks to be split right down the middle – with no clear mandate for either vision.

Its weaker position means the government is more vulnerable to rebellion from its own hard-line backbenchers, which could scupper a Brexit deal. Alternatively, the new administration could seek opposition support. Ultimately, this might soften Brexit but it would be a difficult balancing act, and the risk of a mishap, leading to ‘no deal’, is material.

Domestic policy on the back burner, deficit reduction unlikely

The Conservatives may have to ditch bolder manifesto pledges, like removing the state pension triple lock. More broadly, with spending cuts and tax rises becoming more difficult to pass, we think the budget deficit is unlikely to fall in this parliament. We also expect sterling to continue its descent to 1.20 vs USD as the year progresses. That will keep inflation up, putting pressure on household spending. There is also a risk that political uncertainty will weigh on investment.

HSBC Currency Outlook research reports are available to our regular subscribers. Subscribe now or get a free 5-day trial.

Results: Conservative retain power, just

- The Conservatives won the most seats (318), with Labour in second place (262).

- But Labour has closed the gap – the Conservatives lost 13 seats and Labour won 30 seats, relative to the 2015 election.

- The Conservatives are likely to hang on to power, perhaps requiring an alliance with the Northern Irish DUP. This is in huge contrast to polls from a month ago, which were pointing to a 100-plus Conservative majority. The latest polls were also pointing to a majority, albeit only a modest one (Chart 3).

3. The polls had over-estimated the margin of victory

Source: UK Polling report, HSBC Currency Outlook, BBC

- The Lib Dems have regained some ground following their 2015 election rout. Their seat tally has risen from 8 to 12. But their former leader, Nick Clegg, lost his seat.

- The SNP lost more than 20 seats to all three of the main parties, which will be a disappointment to the party and set back its plans for a second independence referendum. Within that, the SNP has lost two leading figures – the current commons spokesman, Angus Robertson, and the former leader, Alex Salmond.

- In Northern Ireland, the Democratic Unionist Party (DUP) was the largest party, with 10 seats, while Sinn Fein rose to 7 (which it does not traditionally take up).

- With UKIP winning no seats, over 80% of votes went to the Conservatives and Labour: we have seen a return to two-party politics.

What happens next?

The Northern Irish Unionists could come to the rescue

To form a simple majority in the House of Commons, a party needs to win 326 seats. But this is complicated by that fact that the seven MPs from the Northern Irish separatist party, Sinn Fein, do not take their seats in parliament. Adjusting for this, the Conservatives needed 322 seats to form a ‘working majority’.

The Northern Irish Democratic Unionist Party (DUP), who won ten seats, can bolster the Conservatives’ position. Indeed, there has been talk of the DUP propping up a minority Conservative government, if necessary. Both are right-of-centre parties, while we note that the DUP campaigned in favour of Brexit. Some commentators have remarked on an increasing closeness between the parties – the DUP held a champagne reception at last October’s Conservative Party Conference, for example.

A formal coalition between the two parties looks unlikely, rather the DUP’s support might be on an ‘issue-by-issue’ basis. But there seems a strong chance that the DUP will help the Conservatives push through a vote in favour of the Queen’s speech (which outlines the government’s legislative agenda).

In our view, an alternative Labour-led alliance would struggle to form a government. So as long as Conservative and DUP MPs toe-the-line (a big ‘if’ over the course of the parliament as a whole), the government could maintain the confidence of the House.

A more uncomfortable position for the government than before

The election decision seems to have backfired…

Assuming the Conservatives do remain in government, this would be the first minority administration since the 1970s (Chart 4). Without a combination of tight party discipline, an inoffensive domestic agenda and/or corralling support from other parties, the government will struggle to make headway in parliament.

4. A minority administration seems likely

Source: BBC, HSBC Currency Outlook

Specifically, the government is more vulnerable to hardliners within the Conservative party who might wield disproportionate power by withholding support in key votes. A strengthened mandate was a key reason for holding the election. That plan has not succeeded.

Moreover, as the new parliament progresses, the government’s authority could be eroded further through the usual process of by-elections and/or defections – as happened to John Major in the 1990s. In theory, the government should not have to face re-election until 2022, which might enable it to make potentially unpopular concessions in the Brexit negotiations, in order to avoid a ‘cliff edge’ Brexit. But its precarious position means there is no guarantee the government can last the full term.

…and Theresa May’s authority has taken a hit

Theresa May has suffered criticisms for a number of slip-ups on the campaign trail, most notably an apparent U-turn on social care funding pledges in the manifesto, which saw her personal rating fall from 54% to 43% between 20 May and 1 June (YouGov: who would make the best Prime Minister?).

We would not rule out another leadership challenge. If so, the bookmakers think possible challengers include Foreign Secretary Boris Johnson, Chancellor Philip Hammond, Brexit minister David Davis and Home Secretary Amber Rudd.

Labour has performed better than expected, Jeremy Corbyn likely to remain leader

The opposition Labour party, which had been perceived as posing a minimal threat to the government since Jeremy Corbyn’s election as leader in September 2015, will be emboldened by its relative success.

Mr Corbyn’s own rating improved from 15% to 30% over the course of the campaign according to the same YouGov measure. Not only has Labour gained seats, it has won around 40% of the vote, a higher share than under Michael Foot in 1983 (27.6%), Neil Kinnock in 1987 and 1992 (30.8%, 34.4%), Gordon Brown in 2010 (29.0%) or Ed Miliband in 2015 (30.4%) – meaning Tony Blair is the only Labour leader of the last 35 years to have done better.

A wider range of Brexit outcomes is now possible

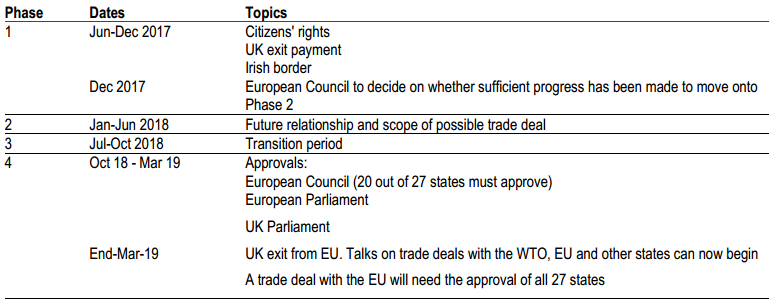

A date of 19 June has been set for formal Brexit negotiations to begin. The logistics of the inaugural day of talks are unclear, but they are likely to be held in Brussels and involve the EU’s chief negotiator, Michel Barnier, and the Brexit Secretary, David Davis.

Looking a little further ahead, the timetable for talks is tight. Mr Barnier has set an end-date for negotiations of October 2018, not the formal Article 50-determined date of March 2019, given the need for national parliaments to ratify any deal.

A major problem for the new government will be that this election offered voters a choice between two very different visions for Brexit: the ‘hard’ Brexit outlined by Theresa May with the door to ‘no deal’ open or Mr Corbyn’s ‘softer’ approach. In the end, the country has offered no clear mandate for either.

The government might need to cross party lines to secure a Brexit deal…

There could be a significant constituency of ‘hard Brexiteers’ on the Conservative back benches. In January, former Conservative leader and prominent Brexit campaigner, Iain Duncan-Smith, said that ‘the right Brexit is clean and swift’ and that agreeing on a transition deal is ‘a big if’. If a transition deal is seen as too ‘soft’, Eurosceptic backbenchers might vote against it.

To guard against this risk, a Conservative government might now try to deliver a (softer) Brexit deal that Labour and the SNP would vote for, in order to fend off its own backbenchers. It is difficult to say what kind of deal Labour and other parties would favour, although Labour’s manifesto does favour continued access to the Single Market and the Customs Union. The government might not need to soften its stance to match Labour’s, given that the only alternative might be ‘no deal’, a scenario Labour wants to avoid. But there might be a middle ground that delivers a Brexit deal which is actually a little softer than a Conservative majority government might have delivered.

…but there is also a higher chance of mishap, leading to a Brexit cliff-edge

But reaching such a middle ground might be difficult. The government might risk heading for a Brexit deal that is too soft for backbench rebels, but too hard for opposition MPs. In this scenario, UK/EU talks might collapse – this ‘no deal’ outcome would lead to a ‘cliff edge’ once the UK formally leaves the EU in March 2019.

Such an outcome might lead to other political ructions. If the government walks away from talks, the opposition might call a vote of no confidence which, if passed, would lead to another general election.

5. The EU’s proposed timetable for Brexit negotiations

Source: European Commission, Financial Times, BBC, HSBC Currency Outlook

A constrained domestic policy agenda

Domestic agenda as squeezed as ever by Brexit…

As before the election, the challenges relating to Brexit talks mean there simply will not be much time for the Conservatives to deal with much else by way of domestic policy reforms. With the government in a weaker position now than before the election, contentious manifesto commitments, such as the pledge to remove the state pension ‘triple lock’ (a commitment opposed by Labour), might well be ditched.

…and deficit reduction will become even more challenging

The more contentious domestic policies tend to be those designed to eliminate the budget deficit. Already in recent months, the government has found it difficult to cut spending and raise taxes. The most notable example was the Chancellor’s U-turn on National Insurance increases following the Budget this March. With the parliamentary arithmetic broadly unchanged, this problem will not go away.

Given our view that the economy is set to grow slowly over the next couple of years, combined with the more challenging fiscal policy environment, our central view is that the government budget deficit, which stood at just over 2.5% of GDP in 2016/17, will not close at all over the course of this parliament.

Economic outlook similar, with more downside risks?

We anticipate higher inflation, weaker household and business spending

We maintain their view that sterling is set to fall further over the course of this year as Brexit talks loom. A weaker path of sterling is likely to continue pushing inflation upwards as businesses pass higher import prices on to consumers. Our forecast is for CPI inflation to peak above 3% later this year. Given downside risks to sterling, risks to this inflation forecast lie somewhat to the upside.

This stronger path of inflation is likely to weigh on household real incomes and spending, which poses a downside risk to economic growth. Although sterling depreciations tend to boost net exports, the impact is likely to be curtailed by the prospect of Brexit, which is a headwind to businesses re-orientating themselves to export-led growth.

Monetary policy will remain dovish

We see no immediate reason to change our forecasts for monetary policy. Given our muted outlook for growth and domestic inflationary pressures (as opposed to a temporary bout of imported inflation), and risks associated with Brexit, we do not expect the Bank of England to raise rates for the whole of this year or next.

HSBC Currency Outlook reports as well as market updates from many investment banks are available to our regular subscribers. Subscribe now or get a free 5-day trial.