Morgan Stanley forex forecast update from Morgan Stanley Global FX Mid-Year Outlook. Subscribe now to access various institutional research reports or get a free 5-day trial here.

Global FX Mid-Year Outlook – Pivot to Europe

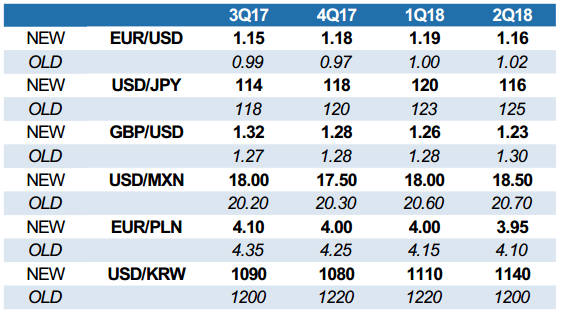

Together with our economics and strategy colleagues we have updated our FX forecasts.

We revise EUR higher as the currency has become positively correlated with growth and political uncertainty has diminished. CHF weakness should come on the back of EUR strength. We project the DXY index to weaken moderately in 2017, but there should be no universal USD trend. While we see USD weakening against most EM and European currencies, we see a higher USD against AUD, CAD, and especially JPY.

Ample liquidity conditions and a continuation of the global growth recovery should keep the yield pick-up trade in place, providing EMFX support. At some point valuations will no longer be as attractive and the US recovery will be in full swing. Higher US capex should increase capital demand and the Fed continuing to hike rates in 2018 could push up real rates, limiting EM’s upside. We see USD rallying across the board from mid-2018.

Favoring CEE amid solid EM outlook: We like CEE currencies, and particularly PLN. Growth continues to recover across the region, boosted by the better prospects within the EU/eurozone more broadly. The next moves for central banks are likely to be toward tightening, while valuations are attractive. Elsewhere, we like MYR on valuation and growth grounds, as well as INR and IDR, while we think MXN will be one of the strongest performers. We expect ZAR to underperform. Risk appetite could fade as we head through 2018.

Our current favorite trades are:

– Long EUR vs USD, JPY, CHF and GBP and short AUDUSD.

– Short EURPLN and short USDMYR.

Major forecast changes

Source: Morgan Stanley forex forecast Research

USD: Mixed performance

Moderate USD weakness: On aggregate, we expect moderate USD weakness for the remainder of this year going into early 2018. We do not expect the USD trend to be universal , with weakness versus EUR and EM but strength versus JPY and AUD in particular. By year-end, we forecast the DXY index (which is 57.6% EURUSD) to weaken by 1.9% and for the Fed’s broad USD index to weaken by 0.8%.

Focusing on the domestic inflation outlook

USD sensitivity to US real yield is high

The global risk outlook has improved notably, suggesting that USD may no longer receive a helping hand from deflationary shocks developing outside the US. Indeed, most of the USD rally from the 2011 low has not been due to strong US fundamentals but instead to conditions elsewhere: the EMU debt crisis, the BoJ taking an aggressive easing course, falling commodity prices and the slowdown in China that triggered capital outflows.

History lessons: Over all these years of seeing USD rallying, the US has remained a place of low real yields, with its capital stock falling, productivity growth staying weak and corporates turning equity into debt to improve their return on equity. Considering these factors, it becomes clear that USD strength has not been home- grown; USD strength was due to external factors. Nonetheless, the rising USD magnified global deflationary pressure into the US, which in turn forced the FOMC to adjust its rate projections repeatedly.

Universal USD strength in 2018? However, broad USD strength should not emerge before earl y 2018, in our view. For USD to rally universally, either US real rates need to rise – which could happen if reforms lift the US economy’s growth potential – or risk appetite needs to reverse, pushing risk-sensitive currencies, most notably EM currencies, lower against USD. By early 2018, we expect EM assets to have reached ambitious valuation levels, in turn getting challenged by markets realizing that ‘the Fed got it right’.

Morgan Stanley forex forecast updates are available to our regular subscribers. Subscribe now or get a free 5-day trial.

US companies are expected to invest

US bank lending expected to pick up

Guided by oil: USD has changed its trading behavior, with many of its past correlations breaking. Most importantly, USD no longer trades inversely to commodity prices. Rising commodity prices have caused USD to move higher and vice versa. This new relationship is best shown in the oil market. The US has emerged as the new swing producer, with the availability of capital, next to the price of oil, determining the pace of oil exploration in the US.

Indeed, oil and commodity markets may pose the biggest risk to our USD call: While moderate commodity weakness may put USDJPY under selling pressure, a bigger oil price decline pushing prices below the marginal cost of production of the US shale industry could push credit spreads wider and equity markets lower. In this case, investors may withdraw from EM markets early.

USD trades increasingly positively with oil

Oil sector’s funding gap

EUR: Bull market in place

Constructive EUR: After years of being bearish on EUR, we conclude that EURUSD traded its lowest post-Lehman level in January, when it moved into the 1.03 handle. We now forecast EURUSD to trade to 1.19 by 1Q18. Political stability and growth-related equity market inflows should boost EUR. We believe that EUR should rise at the same time as global growth. In line with the market, we expect the ECB to start tapering purchases early in 2018. We like to trade EUR crosses higher.

EURUSD is weak on a historical basis

Source: Morgan Stanley forex forecast Research

EUR support from foreigners buying equities

Source: Morgan Stanley forex forecast Research

EUR rises when the US is late-cycle: There are several reasons for this observation. First, the eurozone is a net exporter benefiting from better global demand (with a time lag). Second, the eurozone has been neither a homogenous nor an optimal currency area, experiencing significant internal economic divergence. An incomplete banking union and the absence of a centralized fiscal authority have widened credit spreads, reducing monetary policy effectiveness via widening real rate differentials.

Within an optimal currency area, regional real rates should reflect regional investment and productivity growth. Increasingly, this was not the case within the eurozone, leaving the ECB little choice other than applying monetary policy for its weakest relevant link. Hence, it did not surprise us to see EUR trading at levels indicated by Italian fundamentals instead of those equivalent to broader eurozone fundamentals. The opposite is now occurring for the EUR. Signs that eurozone leaders are moving toward fiscal integration should boost the common currency.

The better global economic backdrop plus booming core EMU economies should help peripheral EMU including Italy, which over time should allow the ECB to break free of its current super-accommodative policy approach, providing EUR support by short-term EUR interest rates breaking higher. Once the German election (September 24) is out of the way, markets will watch whether the new German government makes any concessions, bringing forward EMU’s financial and fiscal integration process. If it does, EUR may move higher than we currently project.

Morgan Stanley forex forecast updates as well as market updates from many investment banks are available to our regular subscribers. Subscribe now or get a free 5-day trial.