ING research reports and a wide range of market analysis from top investment banks are available to our subscribers. Subscribe now or get a free 5-day trial here.

Our top six themes this month

#1 The major risk elections seem to have passed… almost

#2 Why good is not good enough when it comes to Eurozone growth

#3 Why we expect two jumps in EUR/USD over the next two years

#4 Our four scenarios for Trump’s next 100 days

#5 Reflation dashboard: How fiscal stimulus hopes are fading

#6 The latest on the UK General Election, and what it means for Brexit

The big risk elections seem to have passed… Almost

Upcoming elections in UK, France and Germany pose little risk to markets, but don’t forget about Italy

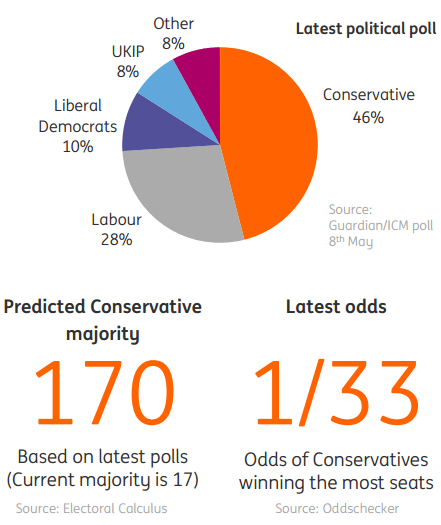

UK general election: 8th June. Market risk? NO

The Conservatives are expected to win with an increased majority, giving PM May a clearer mandate.

French parliamentary elections: 11th June –18th June. Market risk? NO

Following Macron’s defeat of Le Pen, the 577 members of the National Assembly will be elected, with less than 5% of seats projected to be won by politically extreme parties (FN/FG).

German federal election: 24th September. Market risk? NO

The only competition to Merkel’s CDU is the SPD, led by Martin Schulz. Both parties are moderate and there appears to be little threat of a populist victory here.

Italian elections: February 2018. Market risk? YES

Polls suggest anti-EU parties make up almost half of the electorate in Italy. The possibility of the 5* Movement becoming the largest party could unnerve markets.

Despite the politics, the Eurozone recovery is looking good…

Source: ING Research

Private consumption, investments and fiscal policy have all continued to improve during 2017 so far. The Eurozone economy looks to be firing on all cylinders.This recovery is not only the result of favourable external conditions and very accommodative monetary policy, but structural improvements in several countries too. Despite political risk, the Eurozone economy looks to have grown faster than the US and UK in 1Q17 Our forecast of 2% growth for 2017 would be the second strongest year in a decade –and this isn’t just driven by France and Germany, but broader growth across countries: Spain, Portugal, Ireland and the Netherlands are looking strong, and more competitive.

Source: ING Research

…but good isn’t good enough: Structural issues need tackling

Three factors are responsible for limiting structural growth in the Eurozone:

- Declining working age population

- Weak capital stock growth

- Low productivity growth

But there are solutions…

Immigration and reactivation of the hidden workforce could counter the drop in working age population – underemployment is still common.

Looser fiscal policies could help capital stocks to growth by enabling governments to start public investments or incentivise the private sector to invest.

Boosting productivity is the most challenging: until technologies become cheaper and more widespread, weak productivity growth may continue.

ING Economic and Financial Analysis is available to our regular subscribers. Subscribe now or get a free 5-day trial.

The next steps for the ECB now election risks are fading…

We expect the risk assessment and forward guidance to be adjusted at the June meeting

Adjustment of the risk assessment

Forward guidance

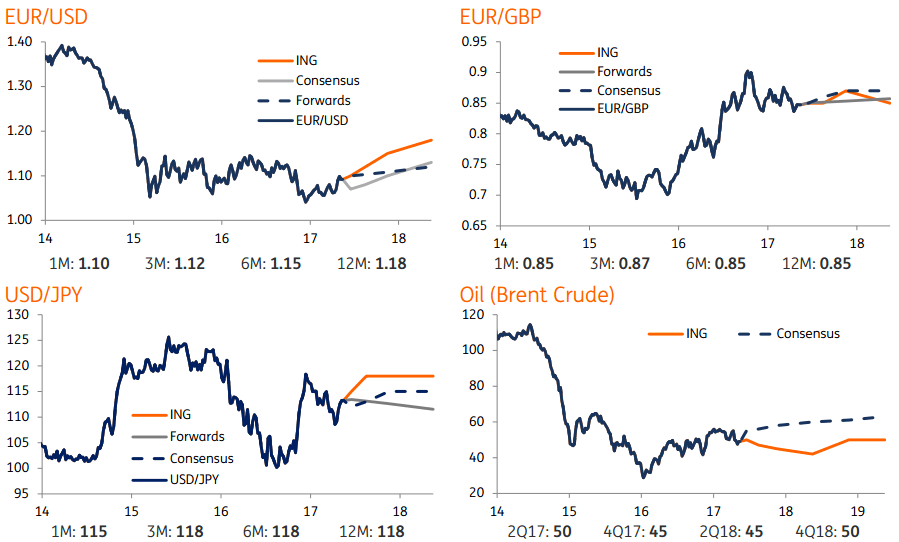

Expect two jumps in EUR/USD as the ECB normalises

One this year and one next year…

Rising long-term yields when the ECB first signals tapering is the main channel through which the Euro should benefit.

This will come as less of a surprise to markets than the Fed’s tapering signal, so the Euro reaction should be less abrupt.

The potential for a 70bp increase in short-term Eurozone yields when markets start positioning for ECB deposit rate hikes will give EUR/USD a boost, particularly given that a gradual Fed tightening cycle is already priced.

Source: ING Research

It’s not just the ECB, there are other stars aligning for the Euro

Source: ING Research

Valuation will become a Euro amplifier

We think that EUR/USD is currently trading around 12% below it’s fair value (based on a range of metrics).

That’s held EUR/USD back from falling considerably below 1.05 this year, despite elevated political risks and excitement about Trump.

We think will only reinforce the upside Euro risk.

Election risk news has a diminishing effect…

There is still a clear risk to the Euro from next year’s Italian election.

But negative political news is having a reduced effect on the Euro, compared to in the Greek crises.

That might be linked to the ECB regaining credibility to “do whatever it takes” to save the Euro.

Trump: The next 100 days…

What to expect on key policy areas over the next year

Source: ING Research

Assessing Trump policy risks

Geopolitical politics replaces protectionism as the negative tail risk

Downshift in expectations given a more watered-down Trump policy regime

4 Trump scenarios over the next 100 days:

- Muddling Through: Trump policy uncertainty prevails leaving global markets directionless

- Reflation Recovery: Trump tax reform plans pass Congress hurdle and provide modest stimulus

- Global Tightening: ECB QE exit & Fed balance sheet shrinking = a perfect storm for long-term yields

- Geopolitical Chaos: Trump foreign policy causes geopolitical fears to escalate in markets

ING Economic and Financial Analysis is available to our regular subscribers. Subscribe now or get a free 5-day trial.

Trump reflation dashboard

Rise and fall in markets shows fading fiscal stimulus hopes

Source: ING Research

Weighing up the dollar positives and negatives…

Our USD outlook can be seen as a balanced seesaw, with supporting factors likely to be offset by medium-term headwinds. Investors will want to see the finer details of Trump’s proposed tax reforms – as well as Congressional backing – before buying into a significantly positive US growth story.

Dollar supportive factors

- Tax repatriation holiday will create $ demand

- Tax reforms (corporate & household tax cuts)

- Deregulation policies

- Infrastructure spending plans ($1trn package)

- US inflation risks underestimated

- Fed balance sheet reduction

Dollar downside factors

Short-term

- Trump “jawboning”

- Geopolitical tensions

Medium-term

- Neutral Fed philosophy

- Structural twin deficit (trade & fiscal)

Fed dots may not need to adjust much to any modest Trump fiscal stimulus and looks fairly consistent with a low interest rate Trump regime.

UK election dashboard: Conservatives look set for big win

Will it make a difference to Brexit? A bit…

The snap election gives PM May greater flexibility to get a transition period agreed, given the next vote won’t be until 2022.

A larger majority may also give her greater confidence to be more realistic/open with the public on the possible economic effects of Brexit.

But the road to Brexit will still be rocky…

The EU’s draft negotiation guidelines, and the fallout from a dinner between the Theresa May and Jean-Claude Juncker, suggest that both sides could hardly be further apart on their Brexit views.

We still think that a positive outcome for both sides is possible given the amount of trade and jobs that are dependent on it.

But there are many obstacles in the road: first of all, the size of the so-called “exit bill”.

We don’t expect a UK rate hike before Brexit talks end…

Economic uncertainty will outweigh concerns about rising prices.

Since the beginning of the year, business surveys have softened and consumer spending has slowed, culminating in a disappointing 0.3%QoQ 1Q17 GDP growth (vs 0.7% in 4Q16). This was significantly weaker than the Bank of England’s 0.6% March forecast and has helped dampen market rate hike expectations.

Inflation is surging due to the lagged effects of sterling’s plunge pushing up the cost of imports. However, domestically generated price pressures are weak, with wage growth having softened and petrol prices dropping. Household inflation expectations are also contained.

Kristin Forbes, the MPC member who actually voted for a rate rise in March will be leaving the committee next month. This will make getting a majority to vote in favour of action more challenging.

Our global forecasts

Get access to ING Research reports (as well as many other institutional research) via our subscription.